As rich-world rate hikes tame inflation at home, they drain capital from vulnerable economies abroad, revealing a global system where decisions are national, but consequences are global

When big economies raise interest rates, loans get costlier, people spend less, and prices fall. The US Federal Reserve raised interest rates 11 times between March 2022 and July 2023, a total increase of 525 basis points. This was among the fastest series of rate hikes in nearly four decades, pushing interest rates from near zero to around 5.25–5.50 percent. It was not acting alone. The European Central Bank and the Bank of England moved in the same direction, at the same time.

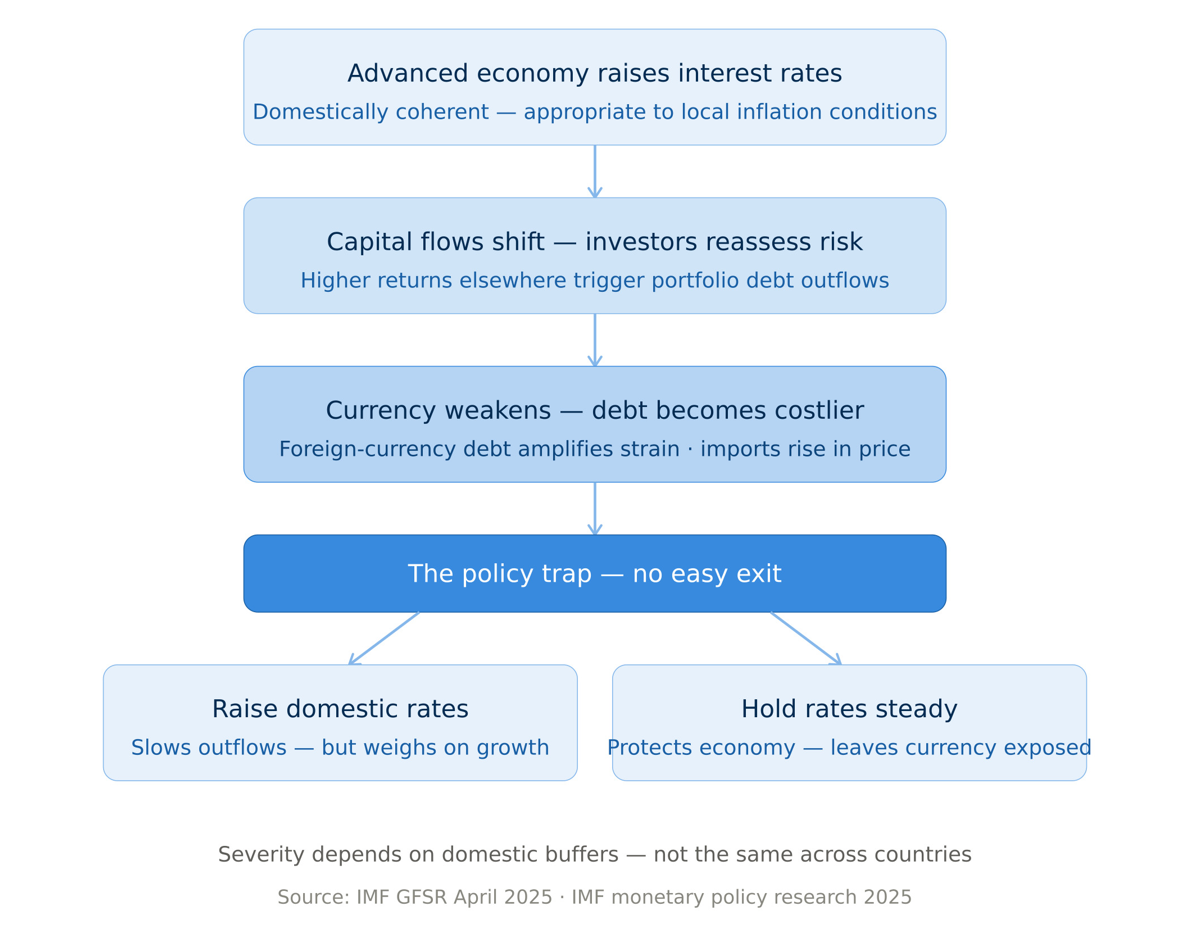

In today's interconnected financial system, capital moves fast and plays no favourites. When rates rise in major economies, money flows toward them and away from everywhere else. Countries already carrying debt or thin reserves feel the hit hardest.

When interest rates rise in major economies, investors holding assets in developing countries face a simple question: is the return still worth the risk? According to the IMF's April 2026 Global Financial Stability Report, money flowing into emerging markets has grown eightfold since the 2008 global financial crisis, reaching around US$4 trillion in total. But these flows have also become very sensitive to changes in global risk. The International Monetary Fund also found that even one sudden jump in market uncertainty, like what happened when the Federal Reserve began raising interest rates in 2022, can lead to money leaving these countries quickly, with outflows of about 1 percent of quarterly GDP on average. When global conditions tighten, money can leave quickly. Countries that entered this period already carrying heavy debts or thin budget reserves had the least room to absorb that kind of shock.

The International Monetary Fund also found that even one sudden jump in market uncertainty, like what happened when the Federal Reserve began raising interest rates in 2022, can lead to money leaving these countries quickly, with outflows of about 1 percent of quarterly GDP on average.

Washington set the pace. Frankfurt followed. The European Central Bank raised its interest rates ten times between July 2022 and late 2023, reaching its highest level since the 2008 financial crisis. The Bank of England did the same, pushing rates from near zero to 5.25 percent in under two years. When all the major economies tighten at once, there is no cushion, no alternative, and no escape. For developing countries, the storm came from every direction at once.

Where a country stands before a crisis largely determines how hard it falls. Ghana, Sri Lanka, and Pakistan each arrived at the edge for different reasons - different spending habits, different governance failures, different economic structures. What they shared was not a common cause but a common condition: too much debt, too little in reserves, and almost no room to manoeuvre when global conditions tightened. All three borrowed when credit was cheap and spent through the pandemic. But the vulnerability was years in the making.

Ghana's problems started with overspending. Public debt had reached around 77 percent of GDP by 2021, built up through years of deficits and overly optimistic revenue forecasts. The fiscal deficit crossed over 11 percent of GDP in 2021 alone, meaning the country was spending far more than it was collecting.

Sri Lanka's problems were different. Reserves had been falling for years as imports consistently outpaced exports. A government ban on chemical fertilisers in 2021 made things significantly worse, damaging harvests, shrinking export earnings, and triggering a food crisis, all while global financing conditions were tightening. The economy contracted 7.3 percent in 2022. Inflation peaked at 69.8 percent in September of that year. The country declared a moratorium on its external debt, its first sovereign default since independence, and required a US$2.9 billion IMF bailout to stabilise.

Pakistan's challenge was structural and long-running. IMF budget analysis showed that in FY2023–24, interest payments alone were expected to exceed PKR 7.3 trillion, in fact exceeding the government's total revenue. This was the result of decades of reliance on external borrowing, a narrow tax base that left the government chronically short of funds, and repeated budget overruns under successive governments.

Three countries, three different stories. All of them ran out of room at the same time. The causes differed; the condition did not. In 2022, developing countries paid US$294 billion in external debt service, and 26 countries with a combined population of 1.3 billion people paid more than they received in new financing that year. The vulnerabilities were home-grown. But the trigger was not.

A key feature of today’s global financial system is that interest rate decisions in places like Washington, Frankfurt, or London can have strong effects on countries far away. This can happen even when those decisions make complete sense for the economies where they are taken. When interest rates swell in major economies, money often moves out of developing countries. Countries with low reserves, high foreign debt, or weaker financial systems feel this the most. The IMF's April 2025 Global Financial Stability Report warned that tighter global conditions can weaken currencies, push down asset prices, and drive capital out of emerging markets, showing how exposed many of these economies still are, even those that have worked hard to improve their policies. This points to a deeper problem in how global monetary policy works. Central banks in rich countries set rates based on their own domestic needs, as they should. But in a world where money moves freely across borders, those decisions don’t stay neatly contained; they spill over and hit poorer countries in ways that are difficult to absorb or avoid.

Frankfurt and London are not incidental to this story. Fourteen countries across West and Central Africa use the CFA franc, a currency pegged to the euro, which means ECB rate decisions directly impact their economies without those countries holding any seat at the table. The Bank of England's cycle did the same for economies carrying sterling-denominated debt. These institutions acted within their mandates. The problem is that their mandates were never designed to account for what happens beyond their borders.

Central banks in rich countries set rates based on their own domestic needs, as they should. But in a world where money moves freely across borders, those decisions don’t stay neatly contained; they spill over and hit poorer countries in ways that are difficult to absorb or avoid.

The costs were distributed unevenly. As Chatham House has noted, emerging markets and developing economies account for around 60 percent of global GDP but hold only 40 percent of the voting power in the IMF. They are impacted the most. They decide the least.

The cost of borrowing for developing countries has gone up over time. They often pay much higher interest on their debt, sometimes several times more than what institutions like the World Bank charge, because investors see them as riskier to lend to. Developing countries paid a record US$1.4 trillion in external debt service in 2023, including US$406 billion in interest payments, making it substantially more expensive to finance schools, hospitals, and infrastructure.

Central banks in wealthy countries set rates for their own economies and answer to their own institutions. That is how it should work. But the problem is not intent, it is design. In a world of open capital flows, where many developing countries hold large amounts of foreign currency debt, shifts in global borrowing costs impact emerging economies. The current governance framework has no reliable way to account for this, and no mechanism to give the most exposed countries a meaningful voice in the institutions managing the response. IMF research has shown that high financing costs, large debt refinancing needs, and shrinking external flows have been squeezing the money available to developing economies for basic spending, even as richer countries began cutting their own rates. The case for reform is not that anyone made the wrong call. It is that the rules were written for a different world.

The most direct levers are quota reform and a rules-based standstill mechanism. Emerging markets are underrepresented in the very institution they turn to in a crisis. Debt relief comes only after the damage is done. Neither reform is simple, but neither is inexcusable. The difficulty is a choice, repeatedly made by those who do not pay for it.

IMF research has shown that high financing costs, large debt refinancing needs, and shrinking external flows have been squeezing the money available to developing economies for basic spending, even as richer countries began cutting their own rates. The case for reform is not that anyone made the wrong call. It is that the rules were written for a different world.

There is a deeper problem that the reform debate has not confronted. The institution that rescues countries in crisis is the same one that sets the terms of recovery. IMF programmes in Ghana, Sri Lanka, and Pakistan all required fiscal discipline measures. Applied to economies that had almost no fiscal space to begin with, those conditions risk amplifying the same vulnerabilities that caused the crisis. The IMF approved a US$2.9 billion Extended Fund Facility (EFF) arrangement for Sri Lanka in 2023. Reform cannot stop at voting shares. It has to address whether crisis response is designed to prevent the next crisis or simply contain the current one. Until it does, the system will keep stabilising countries for the next shock rather than equipping them to absorb it. Global monetary policy crosses borders. Global governance does not. Until that changes, reform will remain in the hands of those with the most votes and the least exposure. That is not a design flaw. It is the design.

Dhani Mehrishi is a Research Intern at the Observer Research Foundation.

The views expressed above belong to the author(s). ORF research and analyses now available on Telegram! Click here to access our curated content — blogs, longforms and interviews.

Dhani Mehrishi is a Research Intern at the Observer Research Foundation. ...

Read More +