Elon Musk's post on India's falling birth rate has renewed focus on the country's sub-replacement fertility trend. The debate now centres on whether India can turn rapid ageing into a silver dividend before its demographic window closes.

Image Source: Getty Images

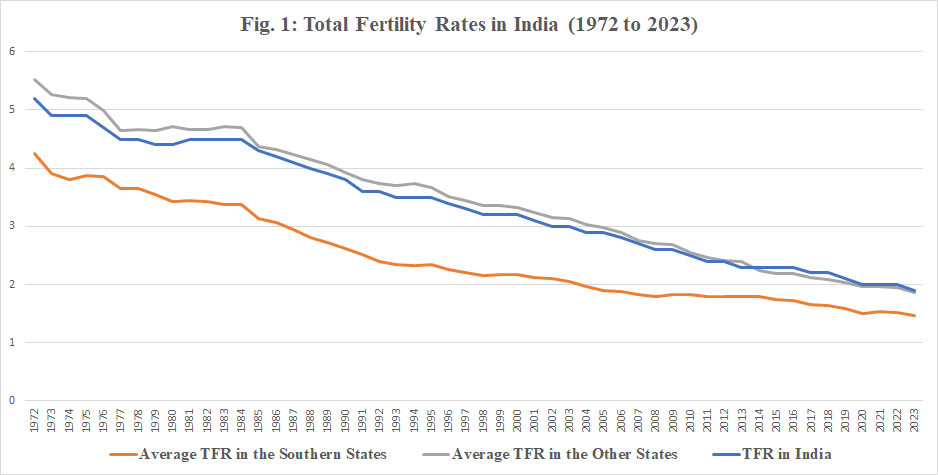

Ever since Elon Musk tweeted on June 6, 2026, about India's declining birth rate, concerns about the nation's Total Fertility Rate (TFR) falling below the replacement level of 2.1 have been discussed in various quarters. The TFR, generally measured as the average number of children a woman would have in her lifetime, is a standardised demographic tool used to project population growth and generational replacement.

However, the information is nothing new — rather, India's present TFR, which stands at 1.9 in 2023, has fallen below the replacement level by 2020. The interesting aspect of this development is that the southern states of India (i.e., Hyderabad, Karnataka, Kerala, Telangana and Tamil Nadu) collectively moved below the replacement level at least two decades ago.

Musk was spot on when he tweeted that "Among those most educated, India's birth rate fell below replacement many years ago", as India's southern states consistently demonstrate higher Human Development Index (HDI) scores and educational attainment than most other Indian states.

Further, according to the NITI Aayog SDG India Index, southern states consistently rank in the "Front Runner" category, driven by strong performance in health, quality education, and poverty reduction.

Given this, India's demographic transition is now being driven less by population growth and more by changes in age structure, fertility, longevity, migration, and regional population dynamics.

The decline in the nation's TFR from 3.5 in the early 1990s to 1.9 in 2023 has resulted in a shrinkage in the proportion of children in the population, while the working-age population (15–64 years) currently accounts for nearly 68% of the total.

India's median age, which was about 26.8 years in 2015, is projected to rise to about 38 years by 2050, reflecting a rapid demographic maturation.

While the southern states are ageing rapidly, states in the Hindi belt, such as Bihar, Uttar Pradesh, and Jharkhand, and parts of the Northeast continue to contribute a disproportionately large share of future population growth and labour force expansion. These regional asymmetries are likely to reshape migration patterns, political representation, labour markets and fiscal transfers over the coming decades.

According to UNFPA projections, India will face one of the world's largest ageing transitions in absolute numbers by 2050.

The country's policy challenge will shift from merely creating jobs for a young population to managing the transition towards a "silver economy" characterised by rising demand for healthcare, pensions, long-term care, and age-friendly infrastructure.

The population aged 60 years and above is projected to rise from about 153 million today to between 319 million and 347 million by 2050, accounting for roughly one-fifth of the country's population. The 80+ age cohort is expected to grow by nearly 279% between 2022 and 2050, making India simultaneously one of the world's youngest and one of its fastest-ageing major economies.

The working-age population is expected to plateau around the early 2040s before beginning to decline, signalling the gradual closure of India's demographic dividend window. Consequently, the country's policy challenge will shift from merely creating jobs for a young population to managing the transition towards a "silver economy" characterised by rising demand for healthcare, pensions, long-term care, and age-friendly infrastructure.

In effect, India's development challenge by mid-century will be to convert its demographic dividend into a productivity dividend before it ages substantially ahead of becoming fully affluent. Is this possible?

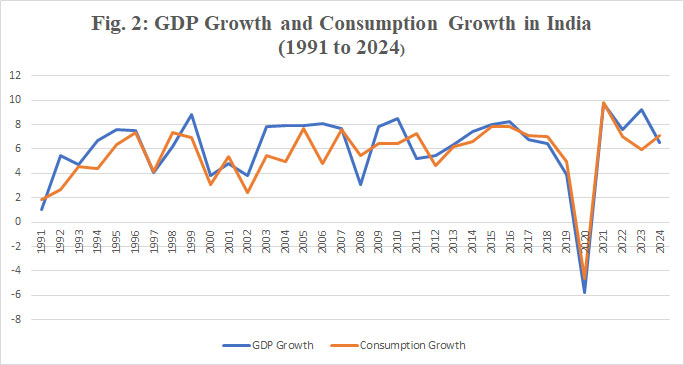

India’s post-reform growth trajectory witnessed the economy’s expansion over the past three decades disproportionately powered by domestic private consumption. This is clearly shown in the graph below, which depicts co-movement between GDP growth and private final consumption growth from 1991 onward.

It should also be noted that during this phase, private final consumption growth, apart from exhibiting co-movement with GDP growth, accounted for 55-62% of GDP, thereby confirming the prevalence of a consumption-driven growth phenomenon.

This surge in private consumption expenditure, characterised by household spending, is driven by higher disposable incomes, a younger demographic, and credit penetration.

A critical element in India's consumption-driven growth story is the bulging youth population, which has not only expanded the working-age populace, enhanced the labour pool and human capital, but also accounted for the bulk of consumption expenditure that boosted growth. On the other hand, there is fairly strong empirical evidence showing that ageing societies tend to experience slower economic growth, though in the modern world, other forces can be in vogue.

A straightforward economic mechanism is that ageing reduces the share of the working-age population while increasing the dependency ratio (the ratio of the dependent population, i.e., children and the aged, to the working-age population) in an economy.

The Paris-based inter-governmental policy forum, OECD, estimates that the old-age dependency ratio will rise from 31% in 2023 to 52% by 2060, while the working-age population (20-64 years) across OECD countries will decline by about 8% during the same period. As a result, average annual per-capita GDP growth in OECD economies is projected to slow significantly and could be 14% lower by 2060 unless countries raise labour-force participation, particularly among women and older workers.

Country experiences reinforce this pattern. Japan is perhaps the most cited example. Its working-age population peaked in the early 1990s and subsequently began shrinking. Over the following decades, Japan experienced persistently low growth, with the IMF identifying demographic ageing and labour-force contraction as major contributors to weaker potential GDP growth. This is also attributed to a decline in private consumption expenditure, which accounts for half of the nation's GDP. At an aggregate level, Japan's population shrank, and the inflation-adjusted (real) wages either declined in recent years, reducing purchasing power.

Current demographic projections indicate that India's demographic dividend is approaching its peak. The growth impetus derived from favourable age structures will gradually weaken, necessitating greater reliance on productivity gains and human capital development. So, in a scenario where India seems to be ageing faster than it is getting richer, Viksit Bharat@2047, which envisages India as a developed nation by 2047, needs a robust backup strategy.

Rather, the loss of a demographic dividend need not imply a loss of economic dynamism.

The challenge, therefore, for Viksit Bharat@2047 is to transform the ageing transition into a "silver dividend" — an economic opportunity arising from healthy, skilled, economically active, and consumption-capable older populations.

Rather than viewing the elderly solely as dependents requiring social support, policy must recognise them as repositories of experience, institutional memory, tacit knowledge, and social capital. In an increasingly knowledge-intensive economy, these assets can continue to generate value long after conventional retirement ages. The silver dividend therefore complements the equity objective of healthy ageing with an efficiency objective centred on productive ageing.

The economic rationale extends beyond labour markets.

As fertility declines and labour-force growth slows, economic expansion will increasingly depend on productivity gains and domestic consumption. Older populations are not merely producers; they are also consumers. Rising life expectancy, better health outcomes, pension incomes, accumulated savings, and growing financial inclusion are creating a large and expanding cohort of consumers whose demand patterns differ from those of younger generations.

Healthcare, wellness, pharmaceuticals, insurance, tourism, leisure, financial services, assisted living, digital services, and age-friendly housing are likely to witness substantial growth as the elderly population expands. In this sense, the silver economy can emerge as a significant source of domestic demand, investment, and employment generation. Rather than a fiscal burden for social security needs, the elderly should be viewed as an increasingly important market segment capable of sustaining consumption-led growth.

A few global north economies that are facing the challenge of skewed demographics and an ageing population are experimenting with raising effective retirement ages, promoting lifelong learning, and introducing policies requiring firms to provide employment beyond the traditional working ages.

Japan, Singapore, South Korea, Germany, and the Nordic nations are prominent examples of countries pursuing the silver dividend.

The 2050 imperative for India is clear: invest in healthy ageing, lifelong skilling, flexible retirement systems, and social protection mechanisms to preserve both the productive and purchasing power of older citizens. In the process, India can transform longevity into a dual economic asset —one that contributes to both supply-side productivity and demand-side consumption.

The silver dividend can thus serve as the bridge between the demographic dividend of the past and the productivity — and consumption — driven growth model required to make India rich.

This commentary originally appeared in India Today.

The views expressed above belong to the author(s). ORF research and analyses now available on Telegram! Click here to access our curated content — blogs, longforms and interviews.

Dr Nilanjan Ghosh heads Development Studies at the Observer Research Foundation (ORF) and serves as the operational and executive head of ORF’s Kolkata Centre. He ...

Read More +