PDF Download

PDF Download

Sreeparna Banerjee, “Exploring Myanmar’s Role in India’s Rare-Earth Elements Security,” ORF Occasional Paper No. 553, Observer Research Foundation, June 2026.

Critical minerals and rare-earth elements (REEs)[a] have become indispensable to modern industrial infrastructure, enabling sectors that underpin both economic and national security. Lithium, cobalt, and nickel, for example, form the backbone of advanced battery systems, while neodymium and dysprosium are essential for permanent magnets in electric motors and wind turbines. Renewable energy infrastructure—from solar PV modules to grid-scale storage—depends heavily on these minerals, as do defence platforms requiring specialised rare earths for jet engines, radar systems, secure communications, and precision-guided systems.

Semiconductors rely on gallium, germanium, and tantalum; consumer electronics incorporate lithium, cobalt, and rare-earth components across virtually all devices. Because disruptions reverberate across multiple sectors simultaneously, these resources are described as ‘critical’. Substitution options remain limited in high-performance magnets and batteries despite research into sodium-ion technologies and alternative magnet chemistries. Thus, global dependence is structural and persistent.

Critical mineral reserves are unevenly distributed across the globe, with only a few countries actively translating their geological potential into production. Chile, Australia, Argentina, and China collectively hold the bulk of global lithium reserves, while the Democratic Republic of the Congo dominates cobalt and copper reserves.[1] Indonesia and Australia together possess a large share of global nickel deposits.[2] REEs, though abundant in the Earth’s crust, are concentrated primarily in China, which holds the largest-known reserves. Many countries—such as Bolivia, Germany, and Mexico—have sizeable lithium resources that remain underdeveloped and have not yet been transformed into economically viable reserves. In response to rising supply risks, several nations are now investing heavily in domestic mining capabilities. These supply-side shifts are reshaping global mineral chains as producer countries seek to meet accelerating global demand.

As the world pivots to clean energy and advanced technologies, control over critical minerals—especially REEs—has become the new frontier of geopolitics. Rare earths are indispensable for manufacturing high-performance magnets used in electric vehicles, wind turbines, smartphones, defence systems, robotics, and advanced medical equipment. Their unique magnetic and thermal properties also make them irreplaceable in the clean energy transition, and global competition for secure access has intensified accordingly.

Against this backdrop, recent reforms to the Mines and Minerals (Development and Regulation) Act, 1957, reflect a phased approach to strengthening India’s critical mineral ecosystem. The 2023 amendment focused on opening the sector by promoting exploration, enabling the auction of critical mineral blocks, and expanding private sector participation. Building on this, the 2025 amendment introduced greater operational flexibility and market-oriented reforms, including easing lease conditions, expanding the scope of exploration institutions, removing restrictions on mineral sales from captive mines, and facilitating mineral exchanges for improved price discovery.

Complementing these legislative measures, the National Critical Minerals Mission (NCMM) was approved by the Union Cabinet on 29 January 2025. Placed under the Ministry of Mines for a period of seven years, it envisages a total outlay of INR 16,300 crore, supplemented by an expected INR 18,000 crore in investments from public sector undertakings. The mission adopts a value chain approach to critical minerals, spanning exploration, mining, processing, recycling, and overseas asset acquisition. As part of the Atmanirbhar Bharat initiative, it seeks to accelerate domestic exploration, streamline regulatory approvals, incentivise private participation, and support the development of processing infrastructure, research, and strategic stockpiles.[3] Together, these measures reflect India’s intent to position itself among countries seeking secure and stable access to critical minerals. Their effectiveness will ultimately depend on financing, implementation, and institutional capacity.

Achieving these ambitions, however, requires more than financial commitment. As global demand rises and competition sharpens, India must convert policy intent into coordinated action across the entire mineral value chain—from exploration and overseas acquisitions to refining, manufacturing, and recycling. Particularly critical are India’s efforts to diversify its supplier base. The push for diversification is driven by two concerns: intensifying geopolitical competition over resource control, and the growing risk of supply chain weaponisation, where dominant actors can restrict access or disrupt flows to exert strategic leverage. The high concentration of refining and processing capabilities in a few countries, particularly China, has heightened these risks, prompting major economies to reconfigure their supply chains.

India possesses considerable domestic potential in critical minerals (Table 1). The country holds around 6.3 percent of global rare-earth resources—about 6.9 million tonnes.[4] Significant deposits of neodymium and praseodymium, along with nearly 35 percent of global beach-sand minerals along its coastline, underscore this potential. India also has substantial graphite reserves and the capability to produce spherical graphite, a key material for battery anodes.

Table 1: Reserves/Resources of REEs in India (as of 1 April 2020, in tonnes)

| State | Total Reserves (A) | Remaining Resources (B) | Total Resources (A+B) |

| All India: Total | - | 459,727 | 459,727 |

| Bihar | - | 1,458.7 | 1,458.7 |

| Gujarat | - | 424,000 | 424,000 |

| Jharkhand | - | 3.59 | 3.59 |

| Karnataka | - | 3,734 | 3,734 |

| Maharashtra | - | 2,090.2 | 2,090.2 |

| Odisha | - | 25,493 | 25,493 |

| Uttar Pradesh | - | 2,948 | 2,948 |

So far, India’s ability to translate this endowment into strategic advantage remains limited. The country continues to be heavily reliant on imports for critical minerals. In 2023, the country met 80 percent of its lithium and cobalt needs, and nearly 90 percent of its REE requirements, through imports (See Table 2).[6] Of these, over 90 percent of rare-earth requirements, particularly processed and refined materials, were sourced from China, highlighting a dependence on it for not only raw materials but also intermediate and finished products. This dependence has deepened in recent years as lithium imports from China grew by some 921 percent between 2023 and 2024, while graphite imports rose by 85 percent from 2022 to 2024. Nickel imports also spiked sharply, increasing by 137 percent in 2024 alone.[7] These trends underscore the structural vulnerabilities within India’s supply chain and the urgent need for diversification and domestic capacity-building.

Table 2: India’s Imports of Rare-Earth Metals (2019-24, in tonnes)

| # | HS CODE DESC. | 2019-20 | 2020-21 | 2021-22 | 2022-23 | 2023-24 | |||||

| 1 | 28053000- Alkali or alkaline earth metals: Rare-earth metals, scandium and yttrium, whether or not intermixed or inter alloyed | Country | Qty | Country | Qty | Country | Qty | Country | Qty | Country | Qty |

| China | 437 | China | 445 | China | 714.5 | China | 709 | China | 699 | ||

| Hong Kong | 34 | Japan | 11 | Japan | 34 | Japan | 42 | Hong Kong | 234 | ||

| Japan | 2 | Sweden | 10 | US | 6.6 | Singapore | 20 | Japan | 192 | ||

| US | 0.57 | US | 4.69 | Hong Kong | 5 | Hong Kong | 20 | Mongolia | 60 | ||

| UK | 0.08 | Hong Kong | 0.05 | Russia | 1 | US | 1.09 | UK | 0.11 | ||

| Others | 0.00 | Others | 0.07 | Others | 0.06 | Others | 0.18 | Others | 0.02 | ||

| Total | 473.65 | Total | 470.61 | Total | 761 | Total | 792 | Total | 1185 | ||

| # | HS CODE DESC. | 2019-20 | 2020-21 | 2021-22 | 2022-23 | 2023-24 | |||||

| 2 | 2846- Compounds, inorganic or organic, of rare earth metals | Country | Qty | Country | Qty | Country | Qty | Country | Qty | Country | Qty |

| Russia | 452 | China | 695 | China | 745 | China | 796 | China | 780 | ||

| China | 434 | Russia | 156 | Japan | 196 | Korea | 150 | Japan | 148 | ||

| Japan | 255 | Japan | 133 | Korea | 93 | Japan | 148 | Korea | 90 | ||

| Germany | 59 | Korea | 91 | Austria | 41 | US | 20 | US | 24 | ||

| Austria | 31 | Austria | 46 | Russia | 40 | France | 14 | France | 19 | ||

| Others | 144 | Others | 129 | Others | 69 | Others | 24 | Others | 24 | ||

| Total | 1375 | Total | 1250 | Total | 1183 | Total | 1153 | Total | 1086 | ||

| REE Total | 1848 | 1721 | 1944 | 1945 | 2270 |

Source: Ministry of Mines 2025[8]

In response, the government has amended the 1957 Mines and Minerals (Development and Regulation) Act in 2023 and 2025. The 2023 amendment aimed to open the sector by promoting exploration, enabling auctions of critical mineral blocks, and increasing private participation. Building on this, the 2025 amendment introduced greater operational flexibility and market-oriented reforms, such as easing lease conditions, widening the role of exploration agencies, allowing mineral sales from captive mines, and supporting mineral exchanges for better price discovery.

The Indian government also launched the National Critical Minerals Mission (NCMM) in January 2025, India’s most ambitious attempt to create a coordinated national framework for securing the supply of 30 critical minerals. The mission brings together efforts in exploration and resource mapping, domestic processing and refining, recycling and circular-economy initiatives, overseas mineral acquisition, and public–private partnerships. Key agencies such as the Geological Survey of India (GSI), Indian Rare Earths Limited (IREL), and Khanij Bidesh India Limited (KABIL) have been tasked with ramping up domestic exploration, expanding refining capabilities, and securing external supplies through bilateral partnerships and overseas asset acquisitions.

India is also advancing self-reliance in critical materials by building a domestic ecosystem for rare-earth permanent magnets, vital for sectors such as electric vehicles, renewable energy, electronics, and defence. In November 2025, the government approved a INR 7,280-crore scheme to establish 6,000 million tons per annum of integrated rare-earth permanent magnet manufacturing capacity across the value chain.[9]

This is complemented by the 2026 Union Budget announcement of dedicated rare-earth corridors in Odisha, Kerala, Andhra Pradesh, and Tamil Nadu to boost mining, processing, research, and manufacturing of critical minerals. These will support the goals of Atmanirbhar Bharat, Net Zero 2070, and Viksit Bharat 2047.

Domestic refining capacity is expanding but remains insufficient. Similarly, weaknesses in processing capabilities further constrain India’s ability to build a competitive critical minerals ecosystem. While India has expertise in base metals, it lacks both domestic mining and advanced processing technologies for lithium, cobalt, and nickel, constraining the development of midstream capacity. The research and development ecosystem remains fragmented, with limited coordination between Council of Scientific and Institutional Research laboratories, Indian Institutes of Technology, universities, and industry, slowing the translation of laboratory innovations into commercially scalable technologies. Poor mine-tailings and waste-management systems also contribute to resource loss, as critical minerals associated with bulk ores—such as REEs and other trace minerals—are often discarded due to inadequate secondary processing infrastructure.[11] At the same time, the exploration and overseas acquisition capabilities of public sector entities remain uneven. While institutions such as the GSI and specialised public-sector undertakings are being mobilised, there is growing recognition of the need to integrate advanced technologies—such as AI-enabled surveys, deep-seated exploration techniques, and modern beneficiation methods—areas where India’s capabilities are still evolving.

Where processing facilities exist—for example, in graphite, titanium, tin, and rare earths—they struggle to achieve high-purity output at commercial scale because of limited economies of scale and a modest domestic market. This creates a cycle of low investment and slow technological upgrades. The sector also faces a notable skill gap, particularly in specialised hydrometallurgical and pyrometallurgical techniques essential for high-purity refining. Policy and regulatory fragmentation add to these challenges; although the NCMM has generated momentum, broader inter-ministerial and state-level coordination remains essential to strengthen India’s processing ecosystem.

Until refining and processing infrastructure becomes both robust and technologically sophisticated, external sourcing will continue to be key to meeting India’s critical mineral requirements.

India is simultaneously expanding its external partnerships to secure critical mineral supplies and strengthening multilateral cooperation. Agreements with countries such as Mongolia and the Democratic Republic of the Congo signal New Delhi’s intent to build long-term overseas access beyond its traditional suppliers.[12] An MoU signed with Mongolia in October 2025 aims to deepen cooperation on minerals such as copper, rare earths, and fluorspar, alongside capacity building in geological exploration and processing.[13]

India’s involvement in plurilateral platforms complements these bilateral efforts. Through the Quad’s Critical and Emerging Technologies Working Group, India works with the United States, Japan, and Australia on supply chain resilience, technology development, and clean-energy standards. As a member of the Mineral Security Partnership and the Indo-Pacific Economic Framework, India participates in global initiatives to create secure, transparent, and sustainable critical mineral supply chains.[14] These engagements, along with others like the India–EU Trade and Technology Council, and the UK–India Roadmap 2030, reinforce India’s alignment with global regulatory standards and its push to build secure and diversified mineral supply chains. Together, these partnerships reflect a strategy centred on balancing upstream access, technology inflows, Environmental, Social and Government (ESG) compliance, and domestic value-chain development.

India’s broader mineral outreach is also taking shape through a layered network of unilateral partnerships. With Australia, the India–Australia Critical Minerals Investment Partnership prioritises lithium and cobalt while embedding cooperation on ESG norms and technology transfer.[15] Engagements with Argentina and Chile focus on lithium extraction and sustainable mining via joint ventures and shared technological expertise. In Africa—particularly Namibia, Tanzania, Zambia, and South Africa—India is exploring upstream investments in cobalt, copper, manganese, and lithium, alongside opportunities to support localised processing.[16]

In the Gulf, partnerships with Saudi Arabia and the UAE emphasise access to industrial minerals and rare earths within wider energy and trade frameworks. Cooperation with Russia is expanding into rare earths and strategic metals despite geopolitical complexities.

Japan remains one of India’s most important partners in critical minerals. Through the Japan–India Clean Energy and Industrial Transition partnership and Japan’s cooperation with KABIL, the two countries are working together on rare-earth supply stability, joint explorations, recycling technologies, and the development of resilient supply chains insulated from geopolitical disruptions.[17]

Together, these partnerships reflect a strategy that combines upstream access to mineral resources with downstream capacity-building through technology transfer, investment, and regulatory alignment. However, they are also shaped by structural constraints within global supply chains, where processing and refining capacities remain concentrated in a limited number of countries, particularly China. This concentration underscores both the urgency of diversification and the limits of external sourcing in the absence of domestic capability expansion.

The approaches of other major economies further illustrate these constraints. Both the United States and Japan have adopted cautious strategies that prioritise sourcing from politically stable and regulated jurisdictions, supported by domestic processing, allied partnerships, and investments in alternative technologies. Concerns over governance, sanctions, and reputational risks have limited their engagement with conflict-affected regions such as Myanmar, highlighting the broader challenges associated with sourcing from such environments.

The vulnerabilities embedded in India’s critical mineral supply chains became starkly visible in April 2025, when China tightened export licensing requirements for REEs and permanent magnets. While export restrictions have increasingly been used by countries to strengthen domestic industries—as seen in Indonesia’s nickel export ban and subsequent expansion of refining capacity—they have also emerged as tools of geopolitical leverage.[18] China’s earlier restrictions on rare-earth exports, as well as controls on gallium, germanium, and graphite to Japan,[b] illustrate how dominant actors can shape global supply dynamics.[19]

The 2025 measures marked an escalation. Beijing’s revised controls require exporters to submit extensive end-use documentation, customer declarations ensuring that materials were not used for defence purposes or re-exported to sensitive markets, and verification of the final application of each shipment. These procedures had extended approval timelines of over 45 days and created a growing backlog of pending Indian applications.[20] With China supplying nearly 80–90 percent of India’s rare-earth magnets, the impact was immediate, disrupting supply chains across electric mobility, wind energy, electronics, medical equipment, and defence manufacturing.[21]

The disruption was most acute in the automotive sector, where rare-earth magnets are indispensable for permanent magnet synchronous motors used in electric and hybrid vehicles. India had imported approximately 540 tonnes of these magnets in the previous fiscal year, more than four-fifths of which came from China.[22] By late May 2025, nearly 30 import requests endorsed by the Indian government remained pending, leaving manufacturers without fresh supplies. Given that most firms maintain only four to six weeks of inventory, production schedules—particularly for upcoming EV models—came under increasing strain. Smaller manufacturers, with limited diversification and lean supply chains, were especially vulnerable.[23]

In October 2025, four Indian companies[c] received conditional approvals to import limited volumes of rare-earth magnets, marking a partial easing of restrictions. However, these approvals remain tightly controlled, contingent on stringent compliance requirements, including detailed end-use verification and non-defence assurances.[24] Rather than signalling a relaxation, they underscore the selective and conditional nature of supply, leaving India exposed to continued uncertainty and potential strategic leverage.

In response, Indian firms have begun exploring alternative suppliers in countries such as Vietnam, Indonesia, Japan, the United States, and Australia. However, building viable supply chains outside China will require time and investment, particularly given the limited processing capacity in many of these locations. In the interim, companies are adjusting production strategies, rationing existing inventories, and, in some cases, prioritising conventional vehicle segments. The government, for its part, has initiated short-term measures such as stockpiling and expedited clearances, while accelerating long-term efforts to expand domestic refining, scale up magnet manufacturing under production-linked incentive (PLI) schemes, and strengthen recycling systems.

The crisis has also prompted a recalibration of India’s external engagements. The longstanding arrangement between IREL and Japan’s Toyota Tsusho—operationalised through Toyotsu Rare Earths India—has effectively been scaled back,[d] with exports curtailed as India prioritises domestic demand.[25] This reflects a broader policy shift toward retaining critical materials for domestic value addition.

What makes the current disruption particularly acute is the structural concentration of rare-earth processing. Unlike the COVID-19 pandemic’s impact on semiconductors—the pandemic had prompted long-term diversification and stockpiling—rare-earth magnet supplies remained largely stable, lulling manufacturers into complacency. With over 90 percent of global refining capacity located in China, short-term substitution options remain extremely limited. The resulting supply shock has begun to affect India’s electric mobility trajectory, with growth projections facing downward pressure.

For India, the 2025 China episode has underscored a fundamental strategic reality: external dependence on highly concentrated supply chains carries systemic risks that cannot be mitigated through ad-hoc adjustments. While diversification and domestic capacity-building are underway, the search for alternative and supplementary sources of supply is becoming increasingly urgent.

Against this backdrop, the question of Myanmar must be situated within India’s wider diversification strategy. While India is expanding partnerships across multiple geographies, gaps remain—particularly in access to HREEs and in identifying geographically proximate sources. India’s search for diversified and resilient supply chains raises an important question: how should it engage with resource-rich but politically complex geographies? Myanmar, with its significant reserves of HREEs, represents one such case—offering potential opportunities alongside substantial risks and constraints. As a complex but strategically relevant node within this broader landscape, Myanmar warrants closer examination despite the political, economic, and operational constraints it presents.

Myanmar’s geological profile is central to understanding its importance within the regional rare-earth ecosystem. The country’s mineral endowment is shaped by two distinct geological zones: the western regions, which are part of the Indo-Burman ranges and share similarities with the Indian subcontinent, and the eastern regions, particularly Kachin and northern Shan, which are geologically linked to the Southeast Asian tin–tungsten and granitic belts extending into southern China.[26] It is within these eastern highland zones that Myanmar hosts significant ion-adsorption clay deposits—formed through the weathering of granitic rocks under tropical conditions—that are enriched in HREEs such as dysprosium and terbium. These deposits are relatively shallow, amenable to low-cost extraction, and have become a major source of HREE feedstock for China’s processing industry. This geological asymmetry—wherein the most strategically valuable deposits are concentrated in conflict-affected eastern regions—adds a critical layer of complexity to any external engagement, including by India. In addition to rare earths, Myanmar also possesses deposits of copper, tin, tungsten, nickel, and gemstones, although the rare-earth sector has gained strategic prominence in recent years due to its role in clean energy technologies and advanced manufacturing.

Myanmar’s mining sector operates under the Myanmar Mines Law 1994, which was amended in 2015 to attract foreign investment by introducing more flexible licensing, joint-venture provisions, and clearer taxation structures. The implementing framework is laid out in the Myanmar Mines Rules 2018, which provide detailed procedures on licensing, mineral production sharing, environmental safeguards, and foreign participation.[27] In theory, the law requires environmental impact assessments, and mandates that all medium- and large-scale mining concessions obtain approval from the Ministry of Natural Resources and Environmental Conservation. In practice, however, enforcement is weak, especially after the 2021 coup. Large parts of Kachin and northern Shan States, where rare-earth extraction occurs, operate outside formal legal frameworks, with mining run by militias, ethnic armed organisations, and business networks aligned with the military. As a result, rare-earth mining largely bypasses the official licensing system, making Myanmar’s formal mining law only partially relevant to the sector. This fragmented and informal governance structure not only limits regulatory oversight but also creates risks for formal international engagement—complicating inter-state cooperation, deterring legitimate investment, and making it difficult to establish transparent and reliable supply chain contracts.

Since the 2021 military takeover, rare-earth mining has expanded at an unprecedented pace across northern Kachin State. Institute for Strategy and Policy-Myanmar reports that the number of operational extraction sites has increased from roughly 130 in 2020 to more than 370 by late 2024. Chipwi Township illustrates this escalation most starkly, with over 2,500 leaching pits identified in 2024.[28] A parallel surge in exports has accompanied this boom: between 2017 and 2024, Myanmar shipped more than 290,000 tonnes of rare-earth materials to China, valued at over US$4.2 billion, 85 percent of it accruing after the coup.[29] By 2023, exports reached US$1.4 billion, firmly positioning Myanmar as China’s dominant external source of HREE, accounting for more than 60 percent of annual imports (See Figure 1).

Before the coup, mining in areas such as Chipwi and Pangwa was primarily overseen by companies linked to the Kachin Democratic Army (NDA-K), a Border Guard Force under the junta. The Myanmar Myo Ko Ko Company[e]—controlled by NDA-K leader Zahkung Ting Ying[f]—played a central role, alongside several local militias and a few Wa-affiliated firms.[30]

The Kachin Independence Army’s (KIA) capture of Chipwi on 30 September 2024 and Pangwa on 20 October 2024 disrupted this trade but also transformed the organisation’s strategic significance.[31] It is no longer only an armed group contesting territory; it now governs resource-rich zones,[g] oversees the taxation of mineral flows, and manages interactions with a major regional power. This evolution is not entirely new. Following its 1994 ceasefire with the Myanmar government, the KIA exercised similar authority over jade production in Hpakant, using resource revenues to consolidate autonomy and build administrative structures.

Figure 1: China’s Imports of RRE (2017-2024)

Source: ISP-Myanmar[32]

China—while closely aligned with the Myanmar military—temporarily shut its border crossings into Kachin Independence Organisation (KIO)/KIA-administered areas in late 2024, using economic pressure as leverage over ethnic armed groups. This led to an abrupt decline of over 80 percent in imports of rare-earth oxide concentrate from Myanmar, according to Chinese Customs data, tightening supply in the global market.[33]

The situation eased somewhat by March 2025, after the KIO reportedly permitted companies to export their stockpiled rare-earth materials while imposing a 35,000 yuan per tonne levy (around US$4,800).[h],[34] Data from Chinese Customs indicates that imports of rare-earth concentrate surged tenfold between March and April 2025, and by May, volumes had nearly returned to levels seen the previous year.[35] Despite its brief duration, the disruption was consequential: Chinese imports from Myanmar collapsed by nearly 89 percent, tightening a supply chain that depends on Myanmar for up to 40–57 percent of input and nearly half of HREE output. The subsequent rebound did little to offset the episode’s impact, which triggered price volatility and exposed structural vulnerabilities in global supply.

In its current role, the KIA increasingly mirrors aspects of the United Wa State Army (UWSA), which regulates tin mining and exports to China. The UWSA’s model—resource governance through informal taxation in exchange for political non-interference—has produced a predictable system of ‘armed commerce’ that Beijing largely accommodates. China may adopt a similar posture towards Kachin-controlled rare-earth extraction. However, key differences remain: the UWSA governs a cohesive, insulated territory, whereas the KIA operates in a socially diverse region with strong Christian networks and an active diaspora that often supports the National Unity Government. This gives the KIA greater global visibility—and exposure—than the UWSA, introducing uncertainty for China as it balances resource access with political sensitivities.

Despite the dip in exports to China during the first nine months of 2025, mining activity in Myanmar is expected to rise as Beijing seeks a more stable and reliable supply chain.[36] Production is therefore expanding beyond Kachin into eastern Shan State: early in 2026, at least 20 new sites were observed in UWSA-controlled Mong Yun and Mong Pawk, and in National Democratic Alliance Army-held areas of Mongyawng Township. Such expansion, however, carries growing risks of environmental and socioeconomic harm. With cross-border impacts increasingly likely, neighbouring countries, including Thailand, are moving to monitor and respond to rare-earth production.

Over the past decade, India–Myanmar relations have deepened, shaped by both strategic and economic priorities. Myanmar occupies a pivotal place within India’s Act East Policy, as the land bridge connecting India to Southeast Asia and the broader Indo-Pacific region. The policy emphasises enhanced connectivity, economic integration, and security cooperation with Myanmar as essential to India’s regional engagement. This strategic focus is reflected in expanding economic ties. India has become Myanmar’s fourth-largest export destination and fifth-largest source of imports, with bilateral trade reaching US$2.1 billion in FY 2024–25.[37] India also ranks as the eleventh-largest investor in Myanmar, with 39 Indian companies holding approved investments worth US$782.82 million.[38]

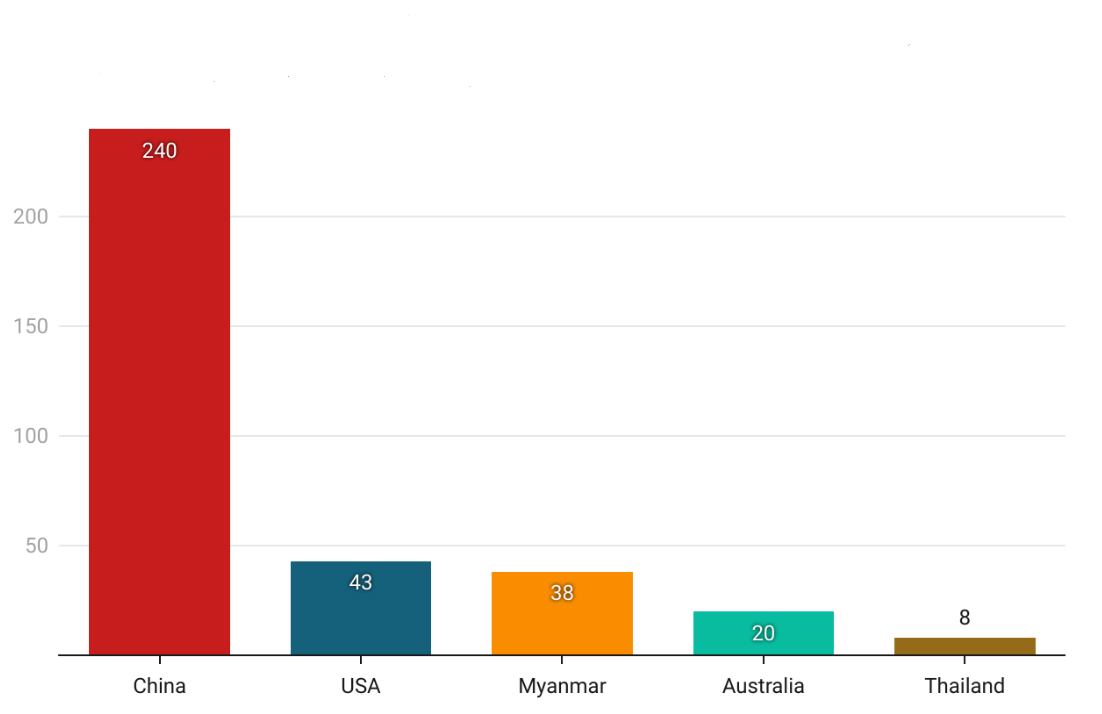

Against this backdrop, Myanmar’s unique geological profile and its central role in the regional rare-earth economy adds a new dimension to India’s regional engagement, aligning strategic connectivity goals with emerging resource security priorities. The International Energy Agency notes that Myanmar is a significant force in global rare-earth mining. In 2024, China was the largest producer of REEs, producing 61 percent, followed by the United States, and then Myanmar at 16 percent, making the Southeast Asian nation the third-largest producer of REEs around the world (See Figure 2).[39]

Figure 2: Top Rare-Earth Producers (2024, in million tonnes)

Source: U.S. Geological Survey[40]

For India, the logic of engagement is driven by its need to reduce dependence on China for critical minerals while assessing feasible, near-term alternatives. This has led to exploratory efforts, including a Geological Survey of India[i] delegation visit to Myanmar in December 2024 to meet officials from the Ministry of Natural Resources and Environmental Conservation.[41] These engagements have reportedly been accompanied by preliminary discussions on assessing rare-earth deposits, including the potential collection and evaluation of HREE samples, although no official confirmation has been provided.[j]

Importantly, the renewed attention to Myanmar’s rare earth reserves has not stemmed from any deliberate diversification strategy on Naypyidaw’s part. Instead, it has arisen largely from external demand—particularly from India and, more recently, the United States—seeking alternative heavy rare earth feedstock as China tightens control over global supply chains. Inside Myanmar, the economic downturn, sanctions, and conflict have pushed various actors—including military-linked conglomerates, border guard forces, and ethnic armed organisations—to explore informal mineral channels. However, these interactions remain fragmented and far from constituting a coherent national policy.[42]

Despite Myanmar’s geological advantages and India’s strategic interest in diversifying its rare earth supply, the feasibility of meaningful engagement remains deeply constrained. Structural, political, and market-driven barriers severely limit India’s ability to access or benefit from Myanmar’s resources in the near term.

China remains the decisive force shaping Myanmar’s rare earth economy, owing to its geographic proximity, political access, and dominance in global refining. Sharing around 700–1000 km of a porous border with Kachin and 1100–1400 km with northern Shan—where most ion-adsorption clay deposits lie—China can source HREE directly from areas controlled by the junta as well as by ethnic armed groups such as the NDA-K and the KIA.

As of 2025, Myanmar supplies over half of China’s imported rare-earth feedstock, and an estimated 70–80 percent of the medium and heavy REE processed in Yunnan originate there. In 2023 alone, China imported more than 30,000 tonnes of mixed rare-earth carbonate from Myanmar, accounting for nearly half of its feedstock for high-value elements like dysprosium and terbium. More than 90 percent of Myanmar’s rare-earth output flows—formally and informally—into Yunnan’s refining and magnet-production ecosystem, giving Beijing near-total leverage over both the upstream extraction and downstream processing chain.

Its reliance on Myanmar did not arise suddenly; it deepened after Beijing tightened domestic environmental regulations around 2015–2016, prompting Chinese companies to shift the most polluting stages of extraction across the border. This trend accelerated after the 2021 coup in Myanmar, when weakened oversight allowed rapid expansion of militia-run mining. Despite intermittent disruptions—including Myanmar’s temporary export ban in 2018 and periodic border closures—Chinese buyers have retained control through informal investment networks and intermediaries linked to armed actors.[43] This entrenched dominance leaves little room for independent external buyers such as India, and severely constrains Myanmar’s ability to diversify its mineral trade.

Even if India sought to source rare earths directly from the Kachin or Shan regions, a number of political factors would severely constrain feasibility. Authority in these areas is fragmented, with control divided among the junta, the KIA, and other armed groups, creating an unpredictable and often volatile operational environment. Most mining zones lack formal regulation, and widespread reports of environmental degradation and human-rights violations raise ethical and governance concerns. The elections held in December 2025 and January 2026 are unlikely to alter these dynamics, as most political parties have been barred from contesting, and the conflict landscape is likely to heighten.

Although India has initiated limited engagement with ethnic armed groups along the India–Myanmar border—particularly with Arakan and Chin actors—it has no precedent for negotiating with non-state armed organisations at this scale, especially in matters related to resource governance. These factors further limit the practical feasibility of direct mineral sourcing from Myanmar’s conflict-affected regions.

India’s geographical proximity to Myanmar should, in principle, offer logistical advantages for rare-earth cooperation. Three key border points form the primary formal gateways between the two countries: Moreh in Manipur, Zokhawthar in Mizoram, and Nampong in Arunachal Pradesh. These crossings could eventually support mineral transport if connectivity initiatives materialise as planned. The Kaladan Multimodal Transit Transport Project, which links India’s eastern ports to Sittwe and onward to Mizoram, offers a potential sea–river–road corridor. At the same time, the India–Myanmar–Thailand Trilateral Highway (IMT-TH) can enable overland movement between Myanmar’s northern resource belts and industrial hubs in India and Southeast Asia.

However, near-term logistical prospects remain limited. Conflict in Sagaing and Chin States has disrupted road networks, and substantial stretches of the Kaladan project will require roads to be built or sections reconstructed before it becomes viable. The securitisation of transport corridors in conflict-affected regions poses further risks to the uninterrupted movement of people or trade. India’s 2023 suspension of the Free Movement Regime—reducing the border movement zone from 16 km to 10 km in 2024 due to security concerns—has restricted civilian and commercial mobility. Infrastructure on the Indian side, particularly in Manipur, has deteriorated amidst prolonged unrest, affecting the functionality of the Moreh–Tamu corridor. Seasonal disruptions, checkpoints run by armed groups, and inconsistent border controls add additional layers of uncertainty.

Thus, while India’s Northeast provides a strong geographical foundation for future mineral supply logistics, current conditions make cross-border transport unreliable, undermining the feasibility of sourcing rare earths from Myanmar in the near term.

Rare-earth mining in Myanmar is associated with severe environmental degradation due to the widespread use of in-situ leaching with ammonium sulfate. The process contaminates the soil, groundwater, and river systems, creating long-term ecological harm that is increasingly documented by civil society networks and international observers. Any Indian purchases routed directly from these mining zones risk reputational damage, particularly as global supply chain scrutiny intensifies. India, which is building climate leadership credentials under its domestic energy transition, cannot afford an association with unsustainable extraction practices that violate international environmental norms.

Even if Myanmar were able to supply India with rare-earth ore, structural constraints on the Indian side would limit the immediate usefulness of such imports. India currently lacks adequate refining capacity for medium and heavy RRE, which are the minerals most abundant in Myanmar’s deposits and the ones most crucial for high-end technologies such as permanent magnets, defence systems, and advanced electronics. As a result, even if raw materials were sourced from Myanmar, India would still need to send them abroad for refining unless domestic capacity is rapidly expanded. Its processing ecosystem, too, remains underdeveloped, and much of the available technology still relies, directly or indirectly, on Chinese expertise or supply chain inputs. Moreover, India’s magnet manufacturing ecosystem remains nascent, with limited capacity to convert refined RREs into high-performance magnets for electric vehicles, wind turbines, and other strategic applications.

This structural gap highlights the importance of parallel investments in refining, processing, and manufacturing to ensure that external diversification efforts translate into real supply chain resilience. However, any rapid expansion of refining and processing capacity would also need to account for the environmental risks associated with rare-earth extraction and separation, including toxic waste generation and groundwater contamination, making strong regulatory oversight and sustainable practices essential to avoid long-term ecological damage.

India’s interest in Myanmar’s rare-earths sector reflects a broader strategic imperative: building resilient, diversified, and future-ready critical mineral supply chains amidst intensifying geopolitical competition. Myanmar’s rare-earth endowments, its proximity to India’s Northeast, and the pivotal role it plays in China’s upstream supply chain make it an important country to monitor—but not yet a viable partner. China’s entrenched dominance, the fragmented political landscape in Kachin and northern Shan, and the reputational risks associated with conflict-linked extraction collectively constrain the prospects for meaningful engagement in the near term. Therefore, Myanmar should be viewed not as an immediate supply option but as a strategically significant variable shaping the regional rare-earths ecosystem.

India’s expanding network of partnerships with Australia, Japan, the US, Canada, the EU, Mongolia, and African states, to name a few, signals a pragmatic shift towards secure and responsible sourcing of critical minerals, while also enabling technology transfer, domestic capacity building, and access to overseas mineral assets. These partnerships are instruments of supply diversification as well as critical to strengthening India’s position across the rare-earths value chain, even as they raise questions about the nature of emerging external dependencies.

At the same time, India faces its own structural limitations in refining, processing, and magnet manufacturing, which must be addressed if external diversification—whether from Myanmar or anywhere else—is to translate into real strategic gains. India’s long-term approach must therefore combine domestic capability building under the NCMM with calibrated external engagement that balances autonomy, environmental responsibility, and geopolitical prudence. As the regional landscape evolves, maintaining awareness, flexibility, and diversified partnerships will be essential for safeguarding India’s mineral security and supporting its clean-energy and technological ambitions.

Sreeparna Banerjee is Associate Fellow, Strategic Studies Programme, ORF.

All views expressed in this publication are solely those of the author, and do not represent the Observer Research Foundation, either in its entirety or its officials and personnel.

Acknowledgement

The author used ChatGPT-5.5 and Grammarly as editorial support tools during the preparation of this paper. The originality, intellectual contribution, analysis, and conclusions of the paper remain entirely the author's own.

[a] Rare earths are a group of 17 elements—scandium, yttrium, lanthanum, cerium, praseodymium, neodymium, promethium, samarium, europium, gadolinium, terbium, dysprosium, holmium, erbium, thulium, ytterbium, and lutetium. They are not rare due to limited availability; they are thinly distributed throughout the Earth’s crust and typically intermixed with other minerals, making substantial deposits difficult to identify and extract economically.

[b] China has repeatedly used such measures, including the 2010 curbs on REE exports to Japan following a maritime dispute and, more recently in 2023, restrictions on gallium, germanium, and high-grade graphite, along with a ban on exporting REE processing technologies. See: https://www.csis.org/analysis/chinas-rare-earth-campaign-against-japan

[c] Companies that have received, or are in the process of securing, Chinese regulatory clearances include Jay Ushin; DE Diamond Electric India; Continental India, the Indian arm of German auto-component major Continental AG; and Hitachi Astemo’s Indian unit. These approvals also cover vendors supplying leading automakers such as Mahindra & Mahindra and Maruti Suzuki, as well as component suppliers to Honda Scooters and Motorcycles. See: https://auto.economictimes.indiatimes.com/news/auto-components/china-eases-rare-earth-magnet-export-restrictions-to-india-a-boost-for-the-auto-industry/126183815#:~:text=China%20has%20begun%20issuing%20licences,licensing%20requirements%20from%20April%204.

[d] Under a 2012 agreement, IREL supplied rare earths to Toyotsu Rare Earths India, a subsidiary of Japan’s Toyota Tsusho, for processing and export to Japan’s magnet industry. In 2024, over 1,000 metric tonnes—around one-third of IREL’s output—were exported under this arrangement. However, in 2025, the Indian government directed IREL to suspend these exports, particularly of neodymium, to prioritise domestic supply. See: https://www.thehindu.com/business/india-moves-to-conserve-its-rare-earths-seeks-halt-to-japan-exports/article69692440.ece.

[e] Around 2019, under the National League for Democracy (NLD)-led administration, several Myanmar-based mining firms applied for permits from the government under the pretext of exploring for other minerals. For instance, Myanmar Myo Ko Ko Company sought a gold mining license from Kachin State’s Mining Department for at least five sites in Chipwi, covering roughly 140 acres. See: https://ispmyanmar.com/wp-content/uploads/2025/06/Rare-Earth-Mining-in-Myanmars-War-Torn-Regions.pdf

[f] The New Democratic Army–Kachin (NDA-K) was formed in 1989 by Zahkung Ting Ying after breaking away from the KIA and later entered a ceasefire with the Myanmar military. In 1994, the regime created Kachin State Special Region-1 under NDA-K control. In 2009, the group was reorganised into the Kachin Border Guard Forces (BGF) under military command, operating from bases in Kan Pike Ti, Pangwa, and Phimaw and controlling parts of Chipwi, Tsawlaw, and Waingmaw. In November 2024, the KIA seized the region, abolishing Special Region-1 and ending NDA-K control. See: https://ispmyanmar.com/wp-content/uploads/2025/06/Rare-Earth-Mining-in-Myanmars-War-Torn-Regions.pdf

[g] Kachin State is rich in other natural resources, including jade, gold, timber, and hydropower potential.

[h] This information, referenced by Reuters, was based on an unverified KIO memo circulated among mining operators. See: https://www.reuters.com/markets/commodities/myanmar-rebel-group-allows-export-rare-earth-inventories-china-sources-say-2025-03-27/.

[i] The GSI has a profound and extensively documented history of geological work in Myanmar, stretching from its establishment in 1851 until the partition of India in 1947. During this period, GSI geologists conducted comprehensive regional surveys, mapping, and mineral exploration, producing foundational data for the country's geological understanding. See: https://www.lyellcollection.org/doi/full/10.1144/m48.1.

[j] Neither the Indian government nor IREL has officially confirmed such activities, and reports of any formal agreement with the KIA have been explicitly denied by Indian authorities. See: https://www.reuters.com/world/china/india-explores-rare-earth-deal-with-myanmar-rebels-after-chinese-curbs-2025-09-10/; https://www.imphaltimes.com/news/india-kia-rare-earth-deal-allegations-denied-by-embassy/amp/

[1] Karthik Bansal and Rajesh Chadha, “Critical Mineral Supply Chains: Challenges for India,” CESP Working Paper 88, February 2025, https://csep.org/wp-content/uploads/2025/02/Critical-Mineral-Supply-Chains-Challenges-for-India-1.pdf.

[2] Bansal and Chadha, “Critical Mineral Supply Chains: Challenges for India.”

[3] Press Information Bureau, Government of India, https://www.pib.gov.in/PressNoteDetails.aspx?id=155158&NoteId=155158&ModuleId=3®=3&lang=2.

[4] “India’s Rare Earth Potential Remains Untapped Amid China’s Dominance,” Chemical Industry Digest, June 14, 2025, https://chemindigest.com/indias-rare-earth-remains-untapped-amid-chinas-dominance/.

[5] Ministry of Mines, “The Indian Minerals Yearbook 2024, Ministry of Mines,” Government of India, January 2026, https://ibm.gov.in/writereaddata/files/17690756386971f3b675b8aFINAL_IMYB2024_as_on_21.01.2026.pdf.

[6] Sunil Kumar, Vibhuti Chandhok, and Rishabh Jain, “Making India a Hub for Critical Minerals Processing,” Council on Energy, Environment and Water, September 16, 2025, https://www.ceew.in/publications/how-can-india-transform-its-critical-and-strategic-minerals-sector-with-domestic-processing-strategy#:~:text=India%20is%20not%20among%20the,rare%20earths%20(CSIS%202025).

[7] Neeraj Singh Manhas, “China’s Stranglehold on Critical Minerals: A Looming Threat to India’s Economic and Strategic Security,” Raksha Anirveda, November 13, 2025, https://raksha-anirveda.com/chinas-stranglehold-on-critical-minerals-a-looming-threat-to-indias-economic-and-strategic-security/#:~:text=The%20Ministry%20of%20Mines%20identified,Effects:%20Economic%20and%20Security%20Perils

[8] Ministry of Mines, Government of India, https://www.pib.gov.in/PressReleasePage.aspx?PRID=2117701®=3&lang=2.

[9] Press Information Bureau, Government of India, https://www.pib.gov.in/PressNoteDetails.aspx?NoteId=157165&ModuleId=3®=3&lang=1.

[10] National Mineral Exploration and Development Trust (NMEDT), Ministry of Mines, Government of India, https://nmet.gov.in/#:~:text=National%20Mineral%20Exploration%20and%20Development,Estimated%20Cost%20of%20the%20Projects.

[11] Kumar, Chandhok, and Jain, “Making India a Hub for Critical Minerals Processing.”

[12] “The Rising Significance of Critical Minerals in Africa,” Indian Council of World Affairs, 2025, https://icwa.in/pdfs/TheRisingSignificanceAfricaWeb.pdf#:~:text=India's%20National%20Critical%20Mineral%20Mission%20(NCMM)%20and,regional%20integration%20under%20frameworks%20like%20the%20AfCFTA.

[13] Ministry of External Affairs, Government of India, https://www.mea.gov.in/bilateral-documents.htm?dtl/40207/Joint_Statement_on_Strengthening_the_Strategic_Partnership_between_India_and_Mongolia_October_14_2025.

[14] Amoha Basrur, “The Quad Critical Minerals Initiative,” Observer Research Foundation, July 19, 2025, https://www.orfonline.org/expert-speak/the-quad-critical-minerals-initiative.

[15] “Australia - India Critical Minerals Investment Partnership,” International Energy Agency, October 15, 2025, https://www.iea.org/policies/17873-australia-india-critical-minerals-investment-partnership.

[16] Anindita Sinh and Constantino Xavier, “Partnerships for Self-Reliance Internationalising India’s Critical Minerals Sector,” CSEP, November 2025, https://csep.org/wp-content/uploads/2025/11/Partnerships-for-Self-Reliance-1.pdf.

[17] Ministry of External Affairs, Government of India, https://www.pib.gov.in/PressReleasePage.aspx?PRID=2162043®=3&lang=2.

[18] John Ryter and Nedal Nassar, “Estimating the Probability of Export Restrictions to Inform Mineral Criticality,” Resources, Conservation and Recycling 226 (2026), https://www.sciencedirect.com/science/article/pii/S0921344925005063.

[19] Gracelin Baskaran and Meredith Schwartz, “The Consequences of China’s New Rare Earths Export Restrictions,” Centre for Strategic and International Studies, April 14, 2025, https://www.csis.org/analysis/consequences-chinas-new-rare-earths-export-restrictions.

[20] Araudra Singh, “India’s Green Shift is Still Made in China,” Frontline, July 8, 2025, https://frontline.thehindu.com/economy/china-rare-earth-export-india-ev-dependence-crisis/article69783024.ece#:~:text=India%20has%20been%20impacted%20by%20Chinas%20rare,Caused%20uncertainty%20around%20production%20schedules%20and%20output.

[21] Singh, “India’s Green Shift is Still Made in China.”

[22] “Rare Earth Magnet Crisis: A Dent in Indian Auto Sector,” The New Indian Express, June 14, 2025, https://www.newindianexpress.com/business/2025/Jun/14/rare-earth-magnet-crisis-a-dent-in-indian-auto-sector#:~:text=India%2C%20which%20sourced%20over%2080,follow%20if%20the%20bottlenecks%20persist.

[23] “Rare Earth Magnet Crisis: A Dent in Indian Auto Sector.”

[24] Anil Sasi, “Indian Companies Bag First Set of Licences for Chinese RE Magnet Imports Amid Signs of Beijing Easing Curbs,” Indian Express, October 31, 2025, https://indianexpress.com/article/business/indian-companies-licenses-chinese-re-magnet-imports-beijing-easing-curbs-10335026/.

[25] “India Moves to Conserve its Rare Earths, Seeks Halt to Japan Exports,” The Hindu, June 13, 2025, https://www.thehindu.com/business/india-moves-to-conserve-its-rare-earths-seeks-halt-to-japan-exports/article69692440.ece.

[26] Khin Zaw et. al., “Introduction to the Geology of Myanmar,” Geological Society of London 48, (2017), https://www.lyellcollection.org/doi/full/10.1144/m48.1.

[27] “Legal and Policy Framework,” Myanmar Centre for Responsible Business, 2018, https://www.myanmar-responsiblebusiness.org/pdf/SWIA/Mining/05-Legal-and-Policy-Framework.pdf.

[29] “Five Key Insights into Myanmar’s Rare Earth,” ISP – Myanmar, March 28, 2025, https://ispmyanmar.com/wp-content/uploads/2025/04/Conflict_Economy_Myanmar_Rare_Earth_ENG.pdf

[30] “Myanmar’s Rare Earths: Cries Behind Critical Minerals.”

[31] Ko Oo, “Rare Earths, Hydropower, and History: Myanmar’s KIA Eyes More Victories in Kachin,” Irrawaddy, October 7, 2024, https://www.irrawaddy.com/opinion/analysis/rare-earths-hydropower-and-history-myanmars-kia-eyes-more-victories-in-kachin.html; Amara Thiha, “Rare Earths and Realpolitik: Kachin Control, Chinese Calculus, and the Future of Mediation in Myanmar,” Stimson, June 24, 2025, https://www.stimson.org/2025/rare-earths-and-realpolitik-future-of-mediation-myanmar/.

[32] “Myanmar’s Rare Earths: Cries Behind Critical Minerals.”

[33] Emily Fishbein and Jauman Naw, “‘Strategic Bargaining Chips’: Kachin’s Rare Rarth Mining Pause,” Frontier Myanmar, August 1, 2025, https://www.frontiermyanmar.net/en/strategic-bargaining-chips-kachins-rare-earth-mining-pause/.

[34] Amy Lv and Lewis Jackson, “Myanmar Rebel Group Allows Export of Rare Earth Inventories to China, Sources Say,” Reuters, March 27, 2025, https://www.reuters.com/markets/commodities/myanmar-rebel-group-allows-export-rare-earth-inventories-china-sources-say-2025-03-27/.

[35] Fishbein and Naw, “‘Strategic Bargaining Chips’: Kachin’s Rare Earth Mining Pause.”

[36] “Myanmar Exported USD 620M Worth of Rare Earths to China in 2025,” ISP-Myanmar, November 27, 2025, https://ispmyanmar.com/pet-03/.

[37] Embassy of India, Yangon, Government of India, https://embassyofindiayangon.gov.in/pages/NDUx#:~:text=Commercial%20Cooperation:%20India%20has%20been,captured%2060%25%20of%20Myanmar's%20market.

[38] Embassy of India, Yangon, Government of India, https://embassyofindiayangon.gov.in/pages/NDUx#:~:text=Commercial%20Cooperation:%20India%20has%20been,captured%2060%25%20of%20Myanmar's%20market.

[39] Melissa Pistilli, “Top 10 Countries by Rare Earth Metal Production,” Investing News Network, March 25, 2025, https://investingnews.com/author/melissa-pestilli/.

[40] Rare Earths, U.S. Geological Survey, January 2024, https://pubs.usgs.gov/periodicals/mcs2024/mcs2024-rare-earths.pdf.

[41] Neha Arora and Naw Betty Han, “Exclusive: India Explores Rare-Earth Deal with Myanmar Rebels After Chinese Curbs,” Reuters, September 10, 2025, https://www.reuters.com/world/china/india-explores-rare-earth-deal-with-myanmar-rebels-after-chinese-curbs-2025-09-10/.

[42] “Rare Earths,” US Geological Survey.

[43] “Unearthing the Cost Rare Earth Mining in Myanmar’s War Torn region,” ISP-Myanmar, June 2025, https://ispmyanmar.com/wp-content/uploads/2025/06/Rare-Earth-Mining-in-Myanmars-War-Torn-Regions.pdf.

The views expressed above belong to the author(s). ORF research and analyses now available on Telegram! Click here to access our curated content — blogs, longforms and interviews.

Sreeparna Banerjee is an Associate Fellow in the Strategic Studies Programme. Her work focuses on the geopolitical and strategic affairs concerning two Southeast Asian countries, namely ...

Read More +