Quick Notes

Social cost of carbon as policy tool: Challenges in the Indian context

Background

A new paper (pre-print) from the National Bureau of Economic Research (NBER), US argues that the economic costs associated with climate change could be six times worse than the previous largest estimates, and 21 times worse than recent values used by the US government. Their estimation of the social cost of carbon (SCC) at US$1,056/tCO2 (per tonne of carbon dioxide) or US$3,872/tC (per tonne of carbon) is way outside the range of existing estimates of the SCC. High estimates of SCC justify increases in spending on mitigating climate change. While the conclusions of the paper are promoted by activist organisations and media outlets, uncertainties over the assumptions and methodology used in the paper to arrive at the high estimates for SCC are yet to be adequately scrutinised. Some of the parameters used in the estimation of the SCC depend on ethical values such as the rate of time preference (discount rate) and the rate of risk aversion both of which can be subjective and lead to an extraordinary range of values for SCC. This raises questions about the use of the SCC for policymaking in India.

The social cost of carbon

SCC compares monetised benefits of policies that result in carbon reductions to their economic costs. Effectively SCC is the present value of future damages associated with an incremental increase (1 metric tonne) in CO2 emissions in a particular year expressed in consumption equivalent terms. In theory, damages from changes in agricultural productivity, human health risks, property damages from increased flood frequencies, and the loss of ecosystem services are included in most SCC models.

An earlier paper based on a sophisticated computational model identified parameters that contribute to uncertainty in SCC. The outcome of the model showed that for lower pure rates of time preference (discount rate plus product of the individual coefficient of risk aversion times the growth rate), the SCC increases and for higher rates, the SCC falls for lower rates because the effect on the discount rate dominates. For assumptions of average time preference and risk aversion, the global SCC was found to be US$12/tCO2 with complete global risk sharing and US$14/tCO2 without risk sharing. When specific equity weights are applied, the SCC ranges from US$2.4/tCO2 in the poorest region (South Asia) to US$1575/tCO2 in the richest.

Another paper estimated SSC by taking into account the future evolution of the economy without the impact of climate change, the Earth system response to emissions of CO2, the economy’s response to climate change, and the net present value of the time series of climate change related future damages arrived at a value of US$ 86/tCO2 for India, the highest, followed by US$48/tCO2 for United States (US) and US$47/tCO2. Brazil, the United Arab Emirates (UAE) and China were next with an SCC of US$24/tCO2. Northern Europe, Canada, and the erstwhile Soviet Union had negative SCC in this model because their current temperatures were below the economic optimum. In this model too the SCC varied considerably depending on the scenario and discount rate. According to the model, damage function uncertainty is a larger contributor to the overall uncertainty. The authors of the paper identified the divergence between country-level shares in CO2 emissions and country-level shares in the SCC as an important reason behind inadequate global carbon mitigation agreements. They concluded that if countries were to price their own carbon emissions at their own SCC, only about 5 percent of the global climate externality would be internalised. However, if the three highest-emitting countries (China, the United States and India) that also have the highest SCC, internalise the negative externalities of emissions by pricing carbon emissions at global SCC levels, it could result in emissions pathways for those countries that are consistent with the 1.5–2°C temperature target.

SCC: Interpretation in India

A paper that analysed the influence of inequality on the SCC concluded that climate and distributional policy cannot be separated. If only one country does not compensate low-income households for disproportionate damages, the social cost of carbon tends to increase globally. The model used in the study puts the SCC for India between US$80-130/tCO2 in 2035 under different assumptions. Higher values of SCC correspond to assumptions of higher inequality within households in the country.

India’s own assessment of country-level SCC is ambiguous. In the last decade, the only publicly available official document that dwells on SCC is the Economic Survey 2016-17. However, the concept of SCC is interpreted differently to justify the use of coal. The document begins by citing Nobel Laurette William Nordhaus who estimated India’s SCC at about US$2.9/tCO2 in 2015 and then proceeds to compare the social cost of coal with the social cost of renewables (RE). The social cost of coal-based power generation is calculated in terms of the number of annual deaths caused by coal-based pollution. Over 110,000 annual deaths attributed to pollution from coal-based power generation are estimated to impose a social cost of US$ 4.6 billion. For RE the social cost is calculated by adding the cost of managing intermittency in power generation by RE, the opportunity cost of land required for RE-based power generation, the cost of stranded assets that RE displaces and the cost of government incentives for RE. The conclusion is that India is justified in its dependence on coal-based power as the social cost of using RE is three times that of coal. The Economic Survey 2016-17 also points out that India’s primary goals are to increase access to energy and close the development deficit gap.

The Economic Survey 2014-15 argued that India had moved from carbon subsidies to carbon taxation as part of its “green action”. Increasing taxes and levies and decreasing subsidies on petrol, diesel and coal justified this statement. Effectively taxes on coal and petroleum products were treated as implicit carbon taxes. In 2014, the implicit carbon tax on petrol was over US$ 140/tCO2 and that on diesel was US$64/tCO2 which were way above the prevailing global norm of US$25-35/tCO2. According to the OECD (Organisation of Economic Cooperation and Development) the effective carbon price in India in 2021 was US$16/tCO2 compared to the US$64/tCO2 a midpoint estimate for carbon costs in 2020, and a low-end estimate for 2030. A country is on a good track to reach the goal of the Paris Agreement to decarbonise by mid-century economically as per OECD classification when it prices carbon at US$64/tCO2 or more in 2020. In May 2024, the total tax levied on a litre of petrol in India was over INR35 and that on diesel was INR28.6. This is roughly equivalent to a carbon tax of $175/tCO2 for petrol and about US$145/tCO2 for diesel. The average taxes per tonne of coal is about INR797/tonne, corresponding to a carbon tax of US$6/tCO2. This implies that the effective carbon tax on petroleum products is higher than what is called for by carbon pricing policies or those set on the basis of SCC.

Challenges

Global, regional and country-level SCC is computed by models using a number of assumptions of which many are uncertain. Ethical values that set intergenerational time discounting and equity weights for rich and poor regions contribute to wide variation in SCC values that could be as large as three orders of magnitude. The damage function or the monetary value of climate damage that underpins SCC models is known to be unknowable. However, the models use assumptions to replace uncertainties and unknowables and the result is expressed in a simple number that suggests a level of knowledge and precision that is non-existent. The seductive power of quantitative analysis and outcomes often precludes comprehensive analysis that includes social and political choices in addressing climate change.

The concept of SCC which is subject to interpretation has received more interest from academics than from policy makers. Studies on academic studies of SCC have shown that authors of primary studies tend to report preferentially which creates an upward bias in the literature. The results also indicated that selective reporting tended to be stronger in studies published in peer-reviewed journals than in unpublished manuscripts.

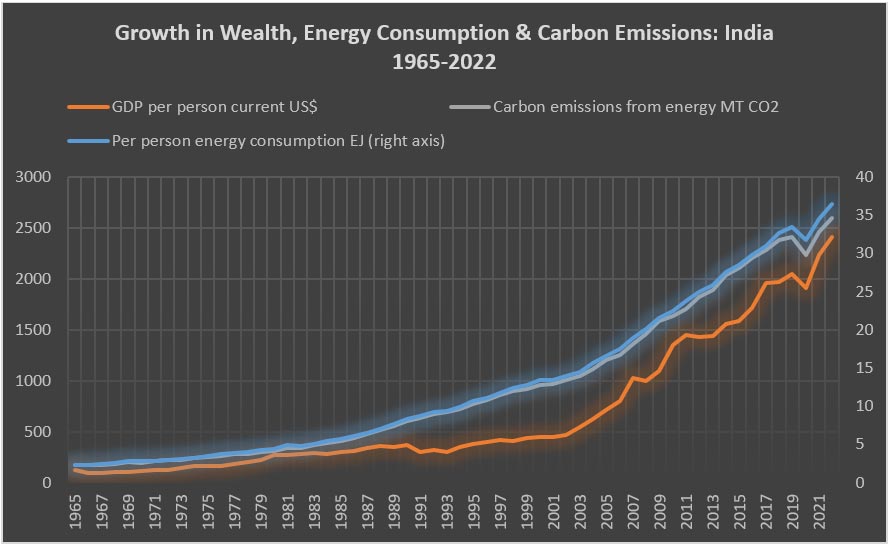

While the fact that the SCC is positive cannot be denied, developing countries such as India have also benefited from the use of fossil fuels (carbon). Since 1960, the global average temperature has increased by 0.75C. In this period, India’s per person energy consumption has increased more than 16-fold resulting in a 20-fold increase in per person gross domestic product (GDP). This has translated into a dramatic increase in life expectancy at birth from about 45 years in 1965 to about 70 in 2022 as well as substantial improvement in quality of life. In the light of social benefits of carbon, it may be wise to weigh disaster narratives quantified with complex computational tools against evident qualitative development outcomes in climate policymaking.

Source: Per person GDP-World Bank; Energy consumption per person & CO2 emission-Statistical Review of World Energy

Monthly News Commentary: OIL

Petrol Exceeds Diesel in Sales Growth

India

Demand

According to the oil ministry’s Petroleum Planning and Analysis Cell (PPAC) data, India’s crude oil import dropped 16 percent in the fiscal year ended 31 March due to lower international rates, but the dependency on overseas suppliers rose to a new high. India imported 232.5 million tonnes (MT) of crude oil, which is refined into fuels like petrol and diesel, in the FY24 (April 2023 to March 2024), almost the same as in the previous financial year. However, it paid $132.4 billion (bn) for the imports in FY24 as against US$157.5 bn import bill in FY23. Import dependence soared to 87.7 percent in 2023-24, up from 87.4 percent. Domestic crude oil production was almost unchanged at 29.4 MT in 2023-24. Besides crude oil, India spent US$23.4 bn on import of 48.1 MT of petroleum products like LPG. It also exported 62.2 MT of products for US$47.4 bn. Petroleum imports as percentage of India’s gross imports (in value terms) stood at 25.1 percent, down from 28.2 percent in 2022-23. Similarly, petroleum exports as a percentage of the country’s gross exports came at 12 percent in 2023-24 as compared to 14 percent in the previous year. India’s fuel consumption rose 4.6 percent to a record 233.3 MT in the year ended 31 March, 2023. This compared with 223 MT consumption in 2022-23 and 201.7 MT in 2021-22. While the country is short in crude oil production, it has a surplus refining capacity that can help export petroleum products like diesel. Against the consumption of 233.3 MT, petroleum product production was 276.1 MT in 2023-24.

According to preliminary data of state-owned firms, India’s petrol consumption soared 7 percent in the first half of April but diesel sales were down 9.5 percent ahead of the onset of a harsh summer season that is set to crank up fuel demand. Petrol sales of three state-owned firms, which control 90 percent of the fuel market, rose to 1.22 MT during 1 to 15 April when compared to 1.14 MT of consumption in the same period last year. While petrol sales were up mostly due to an increase in use of personal vehicles on the back of a price cut, crop harvesting season as well as the onset of summer which will increase the demand for air conditioning in cars is likely to reverse the trend in diesel demand. Petrol and diesel prices were last month reduced by INR2 per litre, ending a nearly two-year-long hiatus in rate revision. Diesel is India’s most consumed fuel, accounting for almost 40 percent of all petroleum product consumption. Transport sector accounts for 70 percent of all diesel sales in the country. Petrol consumption has consistently shown a year-on-year rise, diesel consumption has been on a see-saw - rising in one month and falling in another. Consumption of petrol during the first half of April was 9.2 percent more than in the COVID-marred 1-15 April 2022, and 56.5 percent more than in the first half of April 2020. Cooking gas Liquefied Petroleum Gas (LPG) sales were up 8.8 percent year-on-year at 1.2 MT in 1-15 April 2024. LPG consumption was 15.3 percent higher than in 1-15 April 2022, and 28.3 percent more than in the first half of April 2020.

Retail Prices

Jet fuel or ATF (aviation turbine fuel) price was cut by a marginal 0.5 percent while rates of commercial LPG used by establishments such as hotels and restaurants were slashed by INR31 per cylinder in line with international prices. ATF price was cut by INR502.91 per kilolitre (kl) or 0.49 percent, to INR100,893.63 (US$1210) per kl in the national capital, according to a price notification of state-owned fuel retailers. Rates in Mumbai have been cut to INR94,466.41 per kl from INR94,809.22. Prices differ from state to state depending on the incidence of local taxes. Alongside, oil firms cut the price of commercial LPG by INR30.5 to INR1,764.50 per 19-kg cylinder. Rates of the cooking gas used in domestic households however remained unchanged at INR803 per 14.2-kg cylinder. This is the first reduction in commercial LPG prices since January. Rates had gone up INR14 per cylinder on 1 February and INR25.5 on 1 March. Also, the price of the 5 kg FTL (Free Trade LPG or market priced cooking gas) cylinder has been lowered by INR7.50. IOC, Bharat Petroleum Corporation Ltd (BPCL), and HPCL revise prices of ATF and cooking gas on 1st of every month based on the average price of benchmark international fuel and foreign exchange rate.

Refining

Chennai Petroleum Corp Ltd will build a 180,000 barrels per day (bpd) refinery at Nagapattinam in Southern Tamil Nadu State by the end of 2027, two years later than initially planned. India, the world's third biggest oil consumer and producer, is expanding its refining capacity as it is expected to be the largest driver of global oil demand growth between 2023 and 2030, according to the International Energy Agency. Chennai Petroleum initially planned to complete the refinery by the end of 2025. The company recently changed the capital structure of the joint venture building the project, with its parent company IOC controlling a 75 percent stake and Chennai Petroleum the remainder. Chennai Petroleum operates the 210,000 bpd Manali refinery at Chennai in southern Tamil Nadu state.

Oil India Ltd (OIL) plans to start its 180,000 barrels per day (bpd) Numaligarh refinery in the northeastern state of Assam by December 2025. As per the company it will set up a trading desk as the refinery would process 110,000 bpd of imported crude. The remaining crude requirement would be met through local production. Oil India, which operates exploration and production assets mostly in the northeastern part of the country, would export refined fuels to Bangladesh from the Numaligarh refinery, he said Oil India’s production rose to a record 6.5 million tonne oil equivalent (mtoe) last fiscal year from 6.36 mtoe in fiscal 2023, Rath said. Oil India aims to drill 61 wells this fiscal year compared to 45 in 2023/24.

Imports

India’s net oil import bill could widen to US$101-104 bn in current fiscal from US$96.1 bn in 2023-24 and any escalation in the Iran-Israel conflict could impart an upward pressure on the value of imports, ICRA said. As per ICRA’s calculations, a US$10 per barrel uptick in the average crude oil price for this fiscal pushes up the net oil imports by US$12-13 bn during the year, thereby enlarging the current account deficit (CAD) by 0.3 percent of GDP. Accordingly, if the average crude oil price rises to USD 95 per barrel in FY2025, then the CAD is likely to widen to 1.5 percent of GDP from ICRA’s current estimate of 1.2 percent of GDP for 2024-25. CAD, which is the difference between value of India's imports and exports, is estimated at 0.8 percent in 2023-24. India is more than 85 percent dependent on imports for its needs of crude oil, which is converted into fuels such as petrol and diesel at refineries. ICRA said the value of India’s imports of petroleum crude and products declined by 15.2 percent YoY during April-February of last fiscal, even as volumes rose slightly in this period.

Russia continued to remain the largest supplier of crude oil to India in February with US$3.61 bn worth of supplies, although with a 19 percent drop from the previous month. In January, India imported oil worth US$4.47 bn crude oil from Russia. Russia has been the largest source of crude for India since its invasion of Ukraine in February 2022 sparked western sanctions, prompting it offer deep discounts. India and China have been the biggest beneficiaries of the discounts, which stood at over US$30 per barrel in 2022 but have shrunk over the past year to less than US$5 per barrel. Data from the ministry of commerce and industry showed that oil supplies from Saudi Arabia jumped 67.5 percent to US$2.6 bn taking it to the second position in the list of oil suppliers to India, from US$1.55 bn in January. For most part of the past two years, Iraq has been the second largest supplier to India. It has now slid to the third position with US$2.24 bn worth of supplies in February, 11.6 percent down from US$2.54 bn in January. India’s oil import bill in February 2024 stood at US$13.25 bn, about 10 percent higher from US$12.04 bn in January.

Strategy & Governance

India, the world’s third biggest oil consumer and importer, plans to build its first commercial crude oil strategic storage as part of efforts to shore up stockpiles as insurance against any supply disruption. Indian Strategic Petroleum Reserves Ltd (ISPRL), a special purpose vehicle created by the government for building and operating strategic petroleum reserves in the country, has invited bids for constructing 2.5 MT of underground storage at Padur in Karnataka, according to the tender document. ISPRL had in the first phase built a strategic petroleum reserve in underground unlined rock caverns for storage of 5.33 MT of crude oil at three locations Visakhapatnam (1.33 MT) in Andhra Pradesh and Mangalore (1.5 MT) and Padur (2.5 MT) in Karnataka. Under Phase-II, it intends to build a commercial cum strategic petroleum reserve in underground unlined rock caverns along with associated above ground facilities, including dedicated SPM and associated pipelines (offshore and onshore) for storage of 2.5 MT of crude oil at Padur-II at a cost of INR55.14 bn (US$661 million (mn)). The Phase-I storages were built at government expense. In the tender, ISPRL said the Padur-II will be constructed in a PPP (public-private partnership) model where private parties will design, build, finance, and operate the storage. India, which meets over 85 percent of its oil needs through imports, will use the strategic reserves in any emergency situation like supply disruption or war. Out of the 1.33 MT of storage built at Visakhapatnam, 0.33 MT was a space that was built at the expense and for Hindustan Petroleum Corporation Ltd (HPCL). Of the remaining, HPCL has hired 0.3 MT more and the rest of the storage is to be leased out. At present, crude oil, which is the raw material for producing fuels like petrol and diesel, is not allowed to be exported except through state-owned Indian Oil Corporation (IOC).

Rest of the World

World

The International Energy Agency (IEA) trimmed its forecast for 2024 oil demand growth, citing lower than expected consumption in OECD (Organization for Economic Cooperation and Development) countries and a slump in factory activity. The Paris-based energy watchdog lowered its growth outlook for this year by 130,000 barrels per day (bpd) to 1.2 million bpd, adding that the release of pent-up demand by top oil importer China after easing COVID-19 curbs had run its course. The IEA noted that China’s contribution to the global increase in oil demand is set to weaken from 79 percent in 2023 to 45 percent in 2024 and 27 percent next year. Growth in global supply, the IEA said, will hit 770,000 bpd to reach a total of 102.9 million bpd, led by countries outside the Organization of the Petroleum Exporting Countries and allies (OPEC+).

Africa & Middle East/ OPEC+

Oil companies are flocking to Namibia, excited by the country’s plans to open up a major new frontier basin with recent offshore finds ranking among the largest this century. Namibia, which has yet to produce any oil or gas, has become an exploration hotspot after offshore discoveries by TotalEnergies and Shell and wants to accelerate the milestone of the country’s first output. The southern African country is planning for its first oil production from TotalEnergies' giant Venus field in 2029/2030, its petroleum commissioner Maggy Shino said. In the most recent strike, Portugal’s Galp Energia said it had found at least 10 billion barrels of oil equivalent in its Mopane field, in the largely unexplored Orange Basin.

Iran’s Deputy Oil Minister Morteza Shahmirzaei said that his country was working to ensure that energy exports in the Middle East region are carried out without interruption after an attack on Israel. All countries and players should adhere to the principles of "non-harm" to energy producers to ensure stability, he said. Iran produces more than 3 million bpd of crude oil, about 3 percent of global output, as a major producer within the OPEC.

OPEC oil output fell, a survey found, reflecting lower exports from Iraq and Nigeria against a backdrop of ongoing voluntary supply cuts by some members agreed with the wider OPEC+ alliance. The OPEC pumped 26.42 million bpd, down 50,000 bpd from February, the survey, based on shipping data and information from industry sources, found. A meeting of top OPEC+ ministers kept oil supply policy unchanged and pressed some countries to increase compliance with output cuts, a decision that spurred international crude prices to their highest in five months at nearly US$90 a barrel. A ministerial committee (JMMC) of the OPEC and allies led by Russia, known as OPEC+, met online to review the market and members' implementation of output cuts. Oil has rallied this year, driven by tighter supply, attacks on Russian energy infrastructure and war in the Middle East. Brent crude settled at its highest level since October at US$89.35 a barrel. OPEC+ members, led by Saudi Arabia and Russia, last month agreed to extend voluntary output cuts of 2.2 million bpd until the end of June to support the market. Russian Deputy Prime Minister Alexander Novak said Russia was in full compliance with its commitments to reduce oil supplies as part of the OPEC+ deal.

Exports of Upper Zakum crude from the United Arab Emirates fell sharply in March after ADNOC diverted more supply to its own refinery and boosted shipments of its lighter Murban oil, according to traders, analysts and shipping data. The swap in oil grades at Abu Dhabi National Oil Company (ADNOC)’s Ruwais refinery has tightened medium-sour crude supply in Asia, limiting the number of Upper Zakum cargoes that can be delivered during S&P Global’s price assessment process for Middle East crude Dubai and supporting the benchmark. In 2018, ADNOC invested US$3.5 bn to upgrade its 837,000 bpd refinery to process up to 420,000 bpd of heavier and more sour crude including Upper Zakum. ADNOC started shipping Upper Zakum crude to its refinery in September, with volumes reaching 200,000 to 300,000 bpd in February and March, according to traders.

Russia/Central Asia

The Russian economy ministry has downgraded its forecasts for the country’s crude oil export prices for the next three years to US$65 per barrel. The forecasts, used to compile the federal budget, were cut from previous estimates of US$71.3 per barrel for 2024, US$70.1 for 2025 and US$70 for 2026. Russia has faced myriad sanctions from the West over the conflict in Ukraine, including restrictions on Russian oil purchases as well as a price cap of US$60 per barrel. The downward revision is likely to put more pressure on Russia’s budget, which saw a shortfall of US$6.56 bn, or 0.3 percent of gross domestic product, in the first quarter.

Kazakhstan will compensate for exceeding its oil production quota under the OPEC+ agreement in March, the country's energy ministry said. The ministry said that according to "secondary sources", Kazakhstan produced 131,000 bpd above its quota in March due to weather conditions and heating requirements. It said it would submit a compensation plan to the group’s monitoring committee by 30 April. The operator of Kazakhstan’s giant offshore Kashagan oilfield denied reports of an oil spill near the field and said its facilities were working normally. Globus, an ecological organisation in the Central Asian nation, said that satellite imagery had captured a large oil spill in the northern Caspian Sea near Kashagan. Kashagan, one of Kazakhstan’s largest oil fields, is being developed by the North Caspian Operating Company (NCOC) consortium, which includes Shell Eni, TotalEnergies and Exxon Mobil. The ecology department of Kazakhstan’s Atyrau region, which borders the Caspian, has also said it would conduct a visual inspection and take samples at the oil production site.

North & South America

Technology advances are making it possible for US (United States) shale oil and gas companies to reverse years of productivity declines, but the related requirement to frontload costs by drilling many more wells is deterring some companies from doing so. While overall output is at record levels, the amount of oil recovered per foot drilled in the Permian Basin of Texas, the main US shale formation, fell 15 percent from 2020 to 2023, putting it on par with a decade ago. But new oilfield innovations, which began being implemented more widely last year, have made it possible for fracking to be faster, less expensive and higher yielding.

The Biden administration would not renew a license set to expire early that had broadly eased Venezuela oil sanctions, moving to reimpose punitive measures in response to President Nicolas Maduro’s failure to meet his election commitments. The sweeping sanctions on Venezuela’s oil industry were first imposed by the Trump administration in 2019 following Maduro’s re-election victory, which the US and other Western governments rejected.

According to the US Energy Information Administration (EIA),US oil output from top shale-producing regions will rise in May to the highest level in five months. Production from the top basins will climb by more than 16,000 bpd to 9.86 million bpd, the strongest output since December. US shale oil production, which represents about three-quarters of total US oil output, is rising due to improved well productivity and rebounding activity after a deep freeze in early 2024 forced companies to shut in production. Oil output in the Permian basin, the largest US shale field straddling West Texas and New Mexico, is due to rise by about 11,500 bpd to 6.17 million bpd, the third highest monthly output on record, the EIA said. Production in the Eagle Ford in south-eastern Texas was forecast to climb to 1.16 million bpd, the highest since November, the EIA said. In the Bakken, output was set to increase by 4,800 bpd to 1.25 million bpd, the strongest since December.

US crude oil output is set to grow slightly more than earlier estimates for this year and next, the US EIA said, while also hiking its global and domestic oil price forecasts. US crude production will rise by around 280,000 bpd this year to 13.21 million bpd, and by 510,000 bpd to 13.72 million bpd in 2025, the EIA forecast. It had previously estimated output to rise by 260,000 bpd this year and by 460,000 bpd next year.

Asia Pacific

China increased the pace at which it added crude to inventories in March as the world's biggest oil importer snapped up record imports from Western-sanctioned Russia. A total of 790,000 barrels per day (bpd) were added to China’s commercial or strategic stockpiles in March, up from the 570,000 bpd over the first two months of 2024. Over the first quarter as a whole, China boosted inventories by 670,000 bpd, a figure that to some extent undermines the prevailing market view that China’s oil demand is strong. This is especially the case since China’s crude imports were actually slightly weaker in the first quarter of this year at 11.02 million bpd, down from 11.06 million bpd in the same period in 2023. China doesn't disclose the volumes of crude flowing into or out of strategic and commercial stockpiles, but an estimate can be made by deducting the amount of crude processed from the total of crude available from imports and domestic output. The total crude available to refiners in March was 15.88 million bpd, consisting of imports of 11.55 million bpd and domestic output of 4.33 million bpd. The volume of crude processed by refiners was 15.09 million bpd, leaving a surplus of 790,000 bpd to be added to storage tanks. For the first quarter, the total crude available was 15.31 million bpd, while refinery throughput was 14.64 million bpd, leaving a surplus of 670,000 bpd.

China’s crude oil imports in March fell from high levels a year earlier but remained strong amid a surge in Russian shipments, the General Administration of Customs data showed. Crude imports in March totalled 49.05MT, or about 11.55 million bpd. Total crude imports for the first quarter stood at 137.4 MT, a 0.7 percent increase from last year’s first quarter figure of 136.3 MT. Seaborne imports of Russian crude were expected to reach a record high of 1.816 million bpd in March, according to data from consultancy Kpler, as both state-owned and private refiners snapped up seven tankers of sanctioned Sokol fuel over the course of the month. Natural gas imports for March rose 21.1 percent from a year earlier to 10.76 MT. Prices of LNG for Asia at the end of March were down 26.9 percent on the same period last year, and down 47 percent from their peak in October 2023. Customs data showed exports of refined oil products, which include diesel, gasoline, aviation fuel and marine fuel, were up 9.4% from a year earlier at 6.02 MT.

Pakistan’s government has increased the price of petrol by PKR9.66 per litre amidst inflation. Petrol prices rose to PKR289.41 (US$1.04) per litre from the previous PKR279.75, while high-speed diesel (HSD) decreased by PKR3.32 to PKR282.24 per litre. The adjustment, effective 1 April, was announced by the ministry of finance following a recommendation from the Oil and Gas Regulatory Authority (OGRA). The ministry attributed the change to fluctuations in international petrol and HSD prices, aligning with the government's policy to reflect global market variations domestically. The government maintained petrol prices at PKR 279.75 per litre and reduced HSD prices by PKR1.77 to PKR285.56 per litre. Petrol prices were expected to rise due to increased import premiums and global prices, while HSD prices decreased internationally. Pakistan State Oil (PSO)’s import premium remained at USD6.50 per barrel for HSD, leading to an estimated decrease of PKR1.30 to PKR2.50 per litre. The Pakistan government already levies a petroleum development levy (PDL) of PKR60 per litre, with a target of collecting PKR869 bn (US$3.12 bn) in PDL during the fiscal year.

News Highlights: 1 – 7 May 2024

National: Oil

India’s April fuel demand edges up 6.1 percent year-on-year

7 May: India’s fuel consumption rose by 6.1 percent year-on-year in April, data from the Petroleum Planning and Analysis Cell (PPAC) of the oil ministry showed. India is the world’s third-biggest oil importer and consumer. The data is a proxy for the country’s oil demand. Total consumption totalled 19.86 million metric tonnes (4.85 million barrels per day) in April, up from 18.71 million tonnes last year, data showed. Sales of diesel, mainly used by trucks and commercially run passenger vehicles, rose by 1.4 percent year-on-year to 7.93 million tonnes (MT) in April. Sales of gasoline in April rose 14 percent from the previous year to 3.28 MT. Cooking gas, or liquefied petroleum gas (LPG) sales rose by nearly 10 percent to 2.36 MT, while naphtha sales gained by 3.9 percent to about 1.16 MT, compared with last April, the data showed.

Commercial LPG cylinder price cut INR19, ATF up 0.7 percent

2 May: Oil Marketing Companies (OMCs) reduced price of commercial LPG (liquefied petroleum gas) cylinders, used by businesses such as hotels and restaurants, by INR19 with immediate effect. The price of a 19 kg (kilogram) commercial LPG cylinder will cost INR1,745.50 in Delhi. In April, the price of the same cylinder was reduced by INR30.5. However, there is no change in the price of the domestic LPG cylinder. But OMCs such as Indian Oil Corporation (IOC), Hindustan Petroleum Corporation Limited (HPCL), and Bharat Petroleum Corporation Limited (BPCL) hiked aviation turbine fuel (ATF) prices by 0.7 percent. As per the price notification, ATF price in Delhi has been raised by INR749.25 per kilolitre to INR101,642.88 per kl (kilolitre).

Tripura government imposes restrictions on sale of petrol and diesel

2 May: The Tripura government has imposed restrictions on sale of petrol and diesel from 1 May The disruption in train services has led to a notable decrease in the availability of petrol and diesel in the state, prompting the authorities to regulate the sale of these essential fuels. The restrictions aim to ensure a fair and equitable distribution of petrol and diesel during this period of shortage. Under the imposed restrictions, different categories of vehicles have been allocated specific quantities of petrol and diesel that they can purchase from petrol pumps. Two-wheelers and three-wheelers would get petrol amounting to INR200 per day while four-wheelers it would be INR500 per day.

India’s RIL starts trading US oil setting Brent oil benchmark

2 May: India’s Reliance Industries Ltd (RIL) has made its first foray into trading a type of US (United States) crude oil that underpins the global Brent benchmark in a process run by oil-index publisher S&P Global Commodity Insights. RIL offered a cargo of WTI Midland in the Platts Market on Close process, known as the Platts window. India, the world's third-biggest oil importer and consumer, is looking to diversify its oil supplies as fresh US sanctions on Moscow threaten to dent Russian oil sales to India, the biggest buyer of Russian seaborne crude. India was the top buyer of Russian oil last year after other groups retreated from purchases following Western sanctions on Moscow for its full-scale invasion of Ukraine in February 2022. IL made its first oil purchase from Canada’s new Trans Mountain pipeline last month.

Government cuts windfall tax on crude petroleum

1 May: The government has cut windfall tax on domestically produced crude oil to INR8,400 per tonne from INR9,600 per tonne with effect from 1 May. The tax is levied in the form of Special Additional Excise Duty (SAED). The SAED on the export of diesel, petrol and jet fuel or ATF, has been retained at nil. The new rates are effective from 1 May. India first imposed windfall profit taxes on 1 July 2022, joining a host of nations that tax supernormal profits of energy companies. The tax rates are reviewed every fortnight based on average oil prices in the previous two weeks.

National: Coal

Coal India’s contribution to government exchequer rises 6.4 percent to INR601 bn in FY24

6 May: Coal India Ltd (CIL)’s contribution to the government exchequer increased by 6.4 percent to INR601.40 billion in FY24, over the financial year 2022-23. CIL, which accounts for over 80 percent of domestic coal output, paid INR565.24 billion to the government exchequer in FY23, according to the coal ministry. Coal mining sector has proved to be a big booster for the economic growth of the states that produce fossil fuel. State governments are entitled to receive 14 percent of royalty on the sale price of coal and 30 percent of the royalty as contribution towards the proposed District Mineral Foundations (DMFs)-- which is meant to support project-affected people---and two percent of National Mineral Exploration Trust (NMET) from dry-fuel produced by the coal companies and also the private sector. In case of captive, commercial mines states are also entitled to receive the revenue share offered by the auction holder in a transparent bidding process. CIL’s production and off-take are pegged at 838 MT for FY25.

India’s coal production rises 7.4 percent in April to 78.69 MT

2 May: India’s domestic coal production rose 7.41 percent to 78.69 million tonnes (MT) in April. The country’s coal output was 73.26 MT in the corresponding month of the previous fiscal year. During the last month, Coal India Ltd (CIL) achieved production of 61.78 MT (provisional), registering a growth of 7.31 percent compared to the same period last year when it was 57.57 MT. Additionally, coal production by captive/others last month stood at 11.43 MT (provisional), showing a growth of 12.99 percent from the previous year, which was 10.12 MT. The country’s coal dispatch in April rose to 85.10 MT (provisional) against 80.23 MT in April last fiscal year. CIL accounts for over 80 percent of domestic coal output.

National: Power

India’s power consumption rises 11 percent to 144 bn units in April

1 May: India’s power consumption rose around 11 percent to 144.25 billion units in April as compared to the year-ago period, mainly due increase in temperatures. In April 2023, the power consumption stood at 130.08 billion units, a government data showed. The highest supply in a day (peak power demand) also rose to 224.18 GW (gigawatt) in April 2024 as against to 215.88 GW in April 2023. The power ministry has estimated around 260 GW of peak demand during summer. Experts said the increase in power consumption as well as growth in demand was mainly due to increase in temperatures and increased industrial activities in sectors like steel and power. The demand for power as well as consumption will continue to see robust growth with the onset of summer, they said. The power ministry had estimated the country’s electricity demand to touch 229 GW during summer in 2023, but it did not reach the projected level in April-July due to unseasonal rainfall. Peak supply, however, touched a new high of 224.1 GW in June before dropping to 209.03 GW in July. Industry experts said power consumption was affected in March, April, May, and June in 2023 due to widespread rainfall. They said power consumption grew in August, September, and October, mainly due to humid weather conditions, and also a pick-up in industrial activities ahead of the festive season.

National: Non-Fossil Fuels/ Climate Change Trends

India’s fossil fuel capacity grows 2.44 percent in FY24

3 May: The country’s fossil fuel-based power generation capacity increased 2.44 percent to 243.22 GW in FY24 from 237.27 GW in March 2023. There was a 10.79 percent rise in non-fossil fuel based capacity (renewable energy sources) addition at 190.57 gigawatt (GW) in 2023-24 over 172.01 GW in 2022-23, the government data showed. While the fossil fuel-based capacity includes power generation through coal, lignite, gas and diesel sources, the non-fossil fuel includes power generated from solar, wind and hydropower. The nuclear power capacity addition rose to 8.18 GW from 6.78 GW in the last fiscal year, posting a year-on-year rise of 20.64 percent. In FY24, India’s total power generation capacity rose 6.22 percent to 441.97 GW over 416.06 GW, the data showed.

Renewable energy accounted for 71 percent of India’s new power generation in FY 24

3 May: In India during FY 23-24, renewable energy (RE) contributed more than 70 percent of the 26 GW (gigawatt) of new power generated in the country. India’s total installed energy capacity has now reached 442 GW, with RE comprising approximately 33 percent (144 GW) and hydro contributing 11 percent (47 GW), according to the report by CEEW Centre for Energy Finance (CEEW-CEF). The report further highlights that solar energy, including both grid-scale and rooftop installations, continued to dominate India’s RE capacity addition, constituting approximately 81 percent (15 GW) of the total RE addition in FY24. The wind capacity addition nearly doubled, reaching 3.3 GW compared to 2.3 GW in FY23. Additionally, nuclear capacity (1.4 GW) was added for the first time since FY17. In line with India’s ambitious renewable energy targets, RE auctions soared to a record high, reaching approximately 41 GW of auctioned capacity in FY24.

International: Oil

US EIA cuts 2024 world oil demand growth estimate, hikes output forecast

7 May: World oil demand this year is expected to grow less than earlier forecast and output should expand faster than previous estimates, resulting in a more balanced market, the United States (US) Energy Information Administration (EIA) said. The agency hiked its production forecasts from regions outside the Organization of the Petroleum Exporting Countries (OPEC), while also lowering its expectations of demand from developed economies, according to EIA's Short-Term Energy Outlook (STEO). The EIA expects global oil and liquid fuels consumption to grow by 920,000 barrels per day (bpd) this year to 102.84 million bpd, slightly smaller than the 950,000 bpd growth forecast in its April STEO. Total world crude oil and liquid fuels production was forecast to rise by 970,000 bpd to 102.76 million bpd this year, compared with its previous estimate of an 850,000-bpd increase. The improving market balance also led to a reduction in EIA’s oil prices forecasts for the rest of the year.

Oil production capacity reaches 4.85 million bpd: Abu Dhabi’s ADNOC

2 May: Abu Dhabi oil giant ADNOC’s production capacity has reached 4.85 million barrels per day (bpd), it said, up from the 4.65 million bpd it reported at the end of last year. The announcement comes just ahead of a 1 June meeting in Vienna of the OPEC+ alliance, which groups the Organization of the Petroleum Exporting Countries (OPEC) and allies led by Russia, and of which the United Arab Emirates (UAE) is a key member. The UAE has plans to raise its production capacity to 5 million bpd by 2027 and has long lobbied to raise its output within the OPEC+ agreements. The OPEC producer has seen its target production figure increase in the past year, and it could rise further as it is one of a few countries working to boost production capacity. Its target output within the OPEC+ agreement of 3.219 million bpd covers only two thirds of its actual capacity.

International: Gas

US natural gas output to decline in 2024, while demand rises to record high: EIA

7 May: United States (US) natural gas production will decline in 2024 while demand will rise to a record high, the US Energy Information Administration (EIA) said. EIA projected dry gas production will ease from a record 103.79 billion cubic feet per day (bcfd) in 2023 to 102.99 bcfd in 2024 as several producers reduce drilling activities after gas prices fell to a 3-1/2-year low in February and March. In 2025, EIA projected output would rise to 104.79 bcfd. The agency projected domestic gas consumption would rise from a record 89.10 bcfd in 2023 to 89.31 bcfd in 2024 and 89.64 bcfd in 2025. The agency forecast average US liquefied natural gas (LNG) exports would reach 12.10 bcfd in 2024 and 14.30 bcfd in 2025, up from a record 11.90 bcfd in 2023.

Denmark’s Tyra gas field faces delay, impacts BlueNord guidance

6 May: Denmark’s Tyra natural gas field will only reach peak production in the fourth quarter of this year instead of mid-year due to technical issues with a power transformer, operator TotalEnergies said. While the repair work is ongoing, different options to deliver additional gas volumes to Denmark are being explored, TotalEnergies said. The commissioning of the facilities and gas exports from Tyra continue at present levels, but gas volumes may be redirected to Den Helder, the Netherlands, during remediation, the group said.

Ukraine hopes to boost winter gas storage for Europe by 60 percent

1 May: Ukraine hopes to store around 4 billion cubic metres (bcm) of gas for foreign companies and traders this winter, up 60 percent from last year, despite Russian airstrikes on the country’s energy infrastructure. Storing gas helps Ukraine to collect revenues while providing Europe with additional supply flexibility after the continent cut Russian gas imports because of Moscow’s invasion of Ukraine. Oleksiy Chernyshov, chief executive of Naftogaz, said Russia had attacked the firm’s infrastructure five times since March, in the first such attacks since the war began in February 2022. He said the underground storage was not damaged but Naftogaz was working on strengthening defences as gas pumping facilities above ground are more vulnerable. Underground facilities, mostly in western Ukraine, have a capacity of 31 bcm. He said foreign traders had resumed pumping gas into the storage in recent days. He said volumes were small so far, but he expected them to rise later this year when the heating season approaches.

International: Coal

Met coal imports from Russia up nearly three-fold in last 3 financial years

5 May: Imports of metallurgical coal from Russia have spurted around three-fold in the last three years to around 15.1 million tonnes (MT) in 2023-24 mainly due to lower prices while the same from Australia have declined, according to a research firm. Russia’s share in India’s metallurgical coal imports of 73.2 million tonnes (MT) has risen to around 21 percent from around 8 percent in 2021-22, research firm Big Mint said. The import of metallurgical coal, which includes coking coal and pulverised coal injection (PCI), from Russia, stood at 5.1 MT, accounting for 8 percent of India's total imports of 65.6 MT of the commodity in 2021-22. Metallurgical coal imports from Russia rose to 11.3 MT in 2022-23, accounting for 16 percent of 69.9 MT met coal imports in that year. In 2023-24, met coal imports from Russia were 15.1 MT or 21 percent of total met coal imports of 73.2 MT.

International: Power

US power use forecast to reach record highs in 2024 and 2025

7 May: United States (US) power consumption will rise to record highs in 2024 and 2025, the U.S. Energy Information Administration (EIA) said. EIA projected power demand will rise to 4,103 billion kilowatt-hours (kWh) in 2024 and 4,159 billion kWh in 2025. That compares with 4,000 billion kWh in 2023 and a record 4,067 billion kWh in 2022. With growing demand from data centers and as homes and businesses use more electricity instead of fossil fuels for heat and transportation, EIA forecast 2024 power sales would rise to 1,510 billion kWh for residential consumers, 1,396 billion kWh for commercial customers and 1,048 billion kWh for industrial customers. That compares with all-time highs of 1,509 billion kWh for residential consumers in 2022, 1,391 billion kWh in 2022 for commercial customers and 1,064 billion kWh in 2000 for industrial customers.

US electric utility Sempra's profit falls 17 percent in first quarter

7 May: United States (US) electric utility Sempra Energy posted a 17 percent drop in first-quarter profit as it logged sharply lower revenue from its natural gas operations, although increases in its Texas power business helped cushion the fall. Sempra, which supplies electricity and natural gas to nearly 40 million customers in parts of California, Texas and Mexico, said revenue from its natural gas utilities fell more than 50 percent from a year earlier to US$2.11 billion. Profit at the company’s California utility dropped 5.8 percent, while its electric sales fell to 935 million kilowatt hours (kWh) from 1.6 billion kWh a year ago. Texas is seeing a jump in electricity demand from the proliferation of bitcoin mining, data centers and the electrification of the oil and gas business. The Lone Star state’s grid operator announced that it expected a peak load of 152 gigawatt (GW) in 2030, or nearly double the record.

Ukraine central bank sees average national electricity deficit of 5 percent in 2024-25

3 May: Ukraine’s central bank forecast an average national electricity deficit of about 5 percent this year and next following the latest Russian attacks on Ukraine’s power sector. Over recent weeks, Russia has ramped up missile and drone strikes, damaging most of Ukraine’s thermal power plants along with other power infrastructure. The Ukrainian power system had already been weakened during the first winter of Russia's full-scale invasion, which began in February 2022. Scheduled electricity cut-offs have been introduced in several regions, and Ukraine had to rely on imports from its Western neighbours to meet demand during peak consumption hours. State energy trader 'Ukraine’s Energy Company' said the country imported 225,000 megawatt (MW) of electricity in April, the highest volume so far this year. The central bank expected a more significant electricity deficit from the second quarter of 2024 due to lower water levels for hydropower stations and scheduled repairs at nuclear power stations. Even accounting for imports and partial restoration of generating capacity, the central bank expected a deficit of between 5 percent to 7 percent for the rest of the year. In peak consumption hours the deficit might reach 25-30 percent.

Myanmar grid meeting half of power needs amid conflict

3 May: Myanmar is producing about half of the electricity it needs each day, the junta has said, blaming scant rainfall for hydropower, lower natural gas yields and attacks by its opponents on infrastructure. Rolling power cuts have battered an economy already reeling from unrest sparked by the military’s 2021 coup, most recently causing misery across the country as it bakes in a heatwave. Myanmar’s electricity grid is producing only 2,800 megawatt (MW) of the required 5,443 MW needed each day, according to a statement from the electricity authority released by the junta’s information team. Domestic power production from natural gas was about 446 MW less than the normal daily capacity, and low rainfall had led to a daily shortfall of around 350 MW from hydropower sources, it said. The junta blamed attacks by its opponents for the shortfall in domestic power production.

Shell exits China power market businesses

1 May: Shell has exited China’s power markets as part of CEO (chief executive officer) Wael Sawan’s drive to focus on more profitable operations including its natural gas and oil businesses. Shell decided to exit the power value chain in China, which includes power generation, trading and marketing businesses, it said. The decision was effective from the end of 2023. As part of its drive to save up to US$3 billion in annual costs, Shell has in recent months pulled out of the European retail power business and several offshore wind and low-carbon projects.

International: Non-Fossil Fuels/ Climate Change Trends

Philippines sets goals to double solar, quadruple share of wind in power output

3 May: Philippines aims to increase solar power share to 5.6 percent and wind power share to 11.7 percent in 2030, up from 2.4 percent and 3.1 percent respectively in 2024, according to government presentation, potentially leading to one of the cleanest grids in the region. The archipelago expects that an increased proportion of solar and wind energy will compensate for the decrease in other clean sources like hydropower and geothermal energy, aiming for non-fossil sources to make up 35 percent of power generation by 2030. Philippines is betting on a rapid build out of offshore wind farms, which have high initial costs. Escalating costs amid high inflation have resulted in some developers cancel or postpone projects in the United States (US) and Britain in last year. The country plans to enhance its transmission infrastructure to accommodate the integration of renewables, aiming to add 1,200 MW (megawatt) of nuclear capacity by 2032.

This is a weekly publication of the Observer Research Foundation (ORF). It covers current national and international information on energy categorised systematically to add value. The year 2023 is the twentieth continuous year of publication of the newsletter. The newsletter is registered with the Registrar of News Paper for India under No. DELENG / 2004 / 13485.

Disclaimer: Information in this newsletter is for educational purposes only and has been compiled, adapted and edited from reliable sources. ORF does not accept any liability for errors therein. News material belongs to respective owners and is provided here for wider dissemination only. Opinions are those of the authors (ORF Energy Team).

Publisher: Baljit Kapoor

Editorial Adviser: Lydia Powell

Editor: Akhilesh Sati

Content Development: Vinod Kumar

The views expressed above belong to the author(s). ORF research and analyses now available on Telegram! Click here to access our curated content — blogs, longforms and interviews.